Investors who search beyond the U.S., particularly within the broad and diverse universe of emerging markets, will likely encounter attractive investment opportunities.”

As investors wait for clarity in the wake of President Donald Trump’s sweeping tariff announcements, many are turning their attention beyond the U.S. after more than a decade of being overweight. For the past few years, the U.S. policy mix has increasingly been called into question in key areas including fiscal policy, monetary policy, property rights, the judicial system, and now trade policy. Despite these developments having spanned multiple years and administrations, the recognition of them by investors as measured by the broad underperformance of U.S. assets appears only quite recent (i.e. year-to-date). Against this backdrop, we are seeing more and more investors include emerging markets debt (EMD) and emerging markets equities (EME) more notably into their globally diversified portfolios.

EMD weathered the storm of global macroeconomic uncertainty and performed well during the first quarter of 2025, as currencies broadly strengthened, supported by a weakening U.S. dollar, and a global rally in interest rates.

Q1 2025 Recap

Q1 2025 Recap

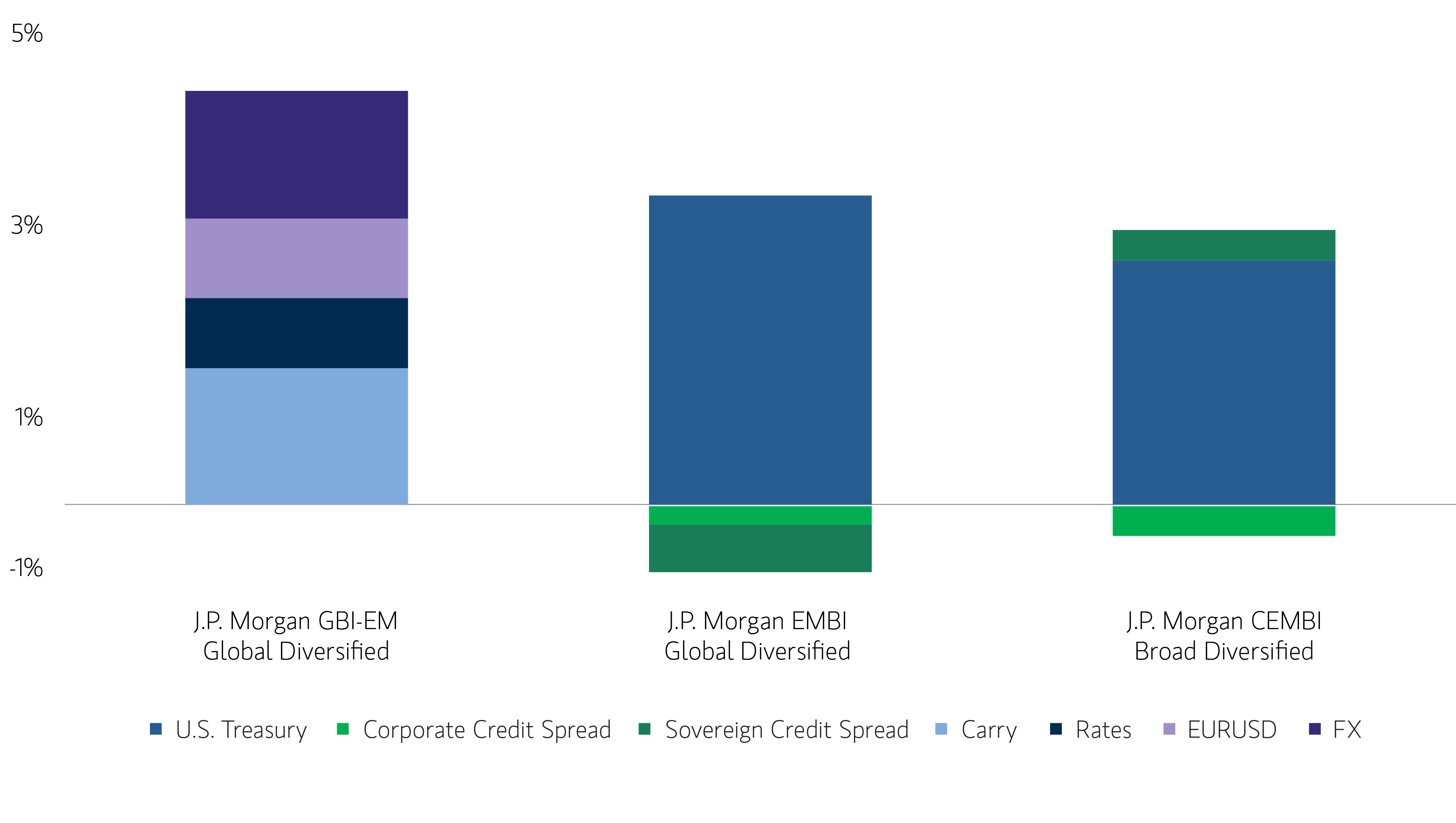

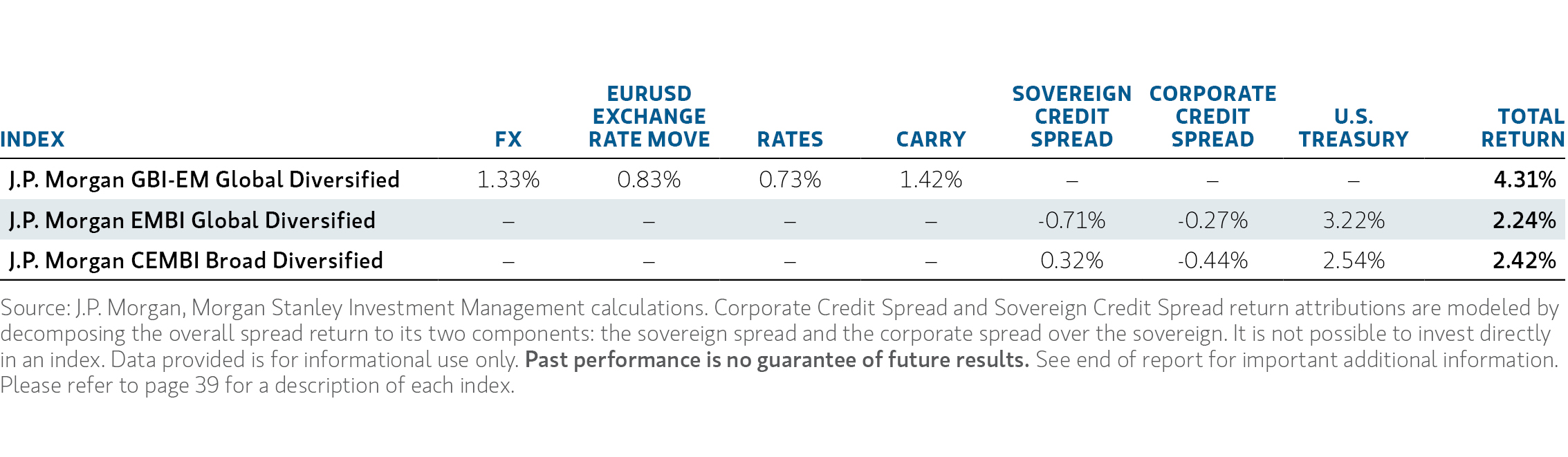

DISPLAY 1

Index Performance Recap

Index Performance Recap

DISPLAY 2

Of course, the first quarter seems like a distant memory in the wake of the market movements since April 2, yet emerging markets (EM) and broader non-U.S. assets have continued to outperform. The combination of the U.S. dollar continuing to weaken through April and global interest rates also declining has been a supportive macro environment for non-U.S. investments including emerging markets.

This outperformance of EM assets relative to the U.S. makes sense. In our view, U.S. policies have moved in a direction less supportive of investment over the past few years. Said another way, the level of economic freedom in the U.S. has been on a declining path. A few examples of a deteriorating policy mix have included the freezing of foreign assets held at the U.S. Fed displaying a decline in respect for property rights, worsening fiscal policy with the running of huge deficits for the past few years even while the economy has generally been running at full employment, and inflation being tolerated above target for an extended period of time representing a decrease in the soundness of money. The latest announcement of tariffs represents a deterioration in free-market trade policy. As experts in sovereign research with a focus on changes in economic policies and institutions across more than 130 countries, the market’s reaction to these U.S. policy developments is no surprise. Should any of the over 130 countries we follow were to announce these types of changes to their policy mix, we would expect a likely increase in the risk-premium associated with investing in that country including lower equity prices, wider credit spreads, and a weakening currency.

So what about emerging markets? From our perspective, it is always worth reminding casual observers that the group collectively referred to as “emerging markets” is really a heterogenous mix of 100+ countries – each with their own economy and direction. As an investment team that prides itself on doing deep, bottom-up analysis on individual countries and companies, this attribute is foundational to what we do every day. That said, there are a few higher-level points worth making as investors seek to determine whether notable increases to emerging markets allocations have merit today.

EM recently had a significant downturn. The period from 2020 through 2022 was a particularly challenging period for all, perhaps none more so than for the poorest countries in the world. The combination of the need for increased fiscal spending in battling COVID-19, the U.S. Federal Reserve’s historically aggressive tightening of monetary policy which increased the “hurdle rate” for investors to take risk elsewhere, and the Russian invasion of Ukraine and the related spike in many commodity prices presented massive challenges. Positioning remains light. Dedicated emerging markets funds have generally experienced notable net outflows since 2022 creating additional pressure on capital markets and leaving many investors under-allocated. Should recent outperformance draw investors back into the space – and we have reason to believe it is – an additional catalyst for performance would likely present. The number of positive, structural reform stories has increased. One result of the prior points, among others, was that many areas of emerging markets capital markets experienced notable stress including a number of sovereign bond defaults. A potential silver lining of this is that, when faced with these challenges, a number of countries have chosen to embark on positive, structural reform paths in order to improve economic outcomes for citizens and attract capital investment. For us as dedicated EM investors, reform stories are what get us really excited and present opportunity for investors.

Of course, not all emerging markets countries are engaged in positive reforms today and some are likely to be more susceptible to changes in U.S. policy than others. As always, a discerning eye is critical – particularly in light of today’s uncertain global macro backdrop.

Bottom Line: Several years of increased volatility and declines in U.S. economic policy has many investors considering reducing overweight exposure to the U.S. and re-sizing those outside the U.S. Given the relatively attractive valuations and the number of positive reform stories, emerging markets stand out for many as a compelling area to do so. The combination of increased diversification, higher yields and the potential to enhance portfolio returns appears compelling. Finally, we believe implementing with an active manager that can differentiate one policy mix from another across countries and companies and beyond benchmarks will likely achieve optimal outcomes for investors.

Featured Insights