Federal Reserve Board1

In March, the Federal Open Market Committee (FOMC) decided to maintain the federal funds target rate at 4.25% to 4.50%. The press release took a dovish tone, highlighting that “uncertainty around the economic outlook has increased.” The release noted that the Federal Reserve (Fed) will “continue reducing its holdings of Treasury securities,” with a notable reduction in the monthly redemption cap on Treasury securities from $25 billion to $5 billion. The path ahead remains uncertain as the Fed remains data dependent in considering further rate cuts.

European Central Bank1

The European Central Bank (ECB) Governing Council lowered the key deposit rate by 25 basis points at the conclusion of its policy meeting in March to 2.50%. The ECB credited the cut to the “disinflation process” being “well on track.” On inflation, wage growth was high and prices in certain sectors continue to adjust to past inflation surges with a substantial delay. Most measures of underlying inflation suggest that inflation will settle at around the Governing Council’s 2% medium-term target on a sustained basis. The path ahead remains uncertain as the Governing Council is not pre-committing to a particular rate path and remains data dependent.

Bank of England

The Bank of England (BoE) Monetary Policy Committee (MPC) voted 8-1 to maintain the Bank Rate at 4.50% at the conclusion of its March meeting. One member preferred to reduce Bank Rate by 0.25% to 4.25%. The BoE has adopted a gradual approach in removing policy restraint in the absence of material developments. Twelve-month CPI inflation increased to 3.0% in January from 2.5% in December; domestic inflationary pressures are moderating but remain somewhat elevated. Monetary policy will remain restrictive for sufficiently long until inflation sustainably returns to its 2% target. The committee remains cautious in determining the appropriate degree of monetary easing.

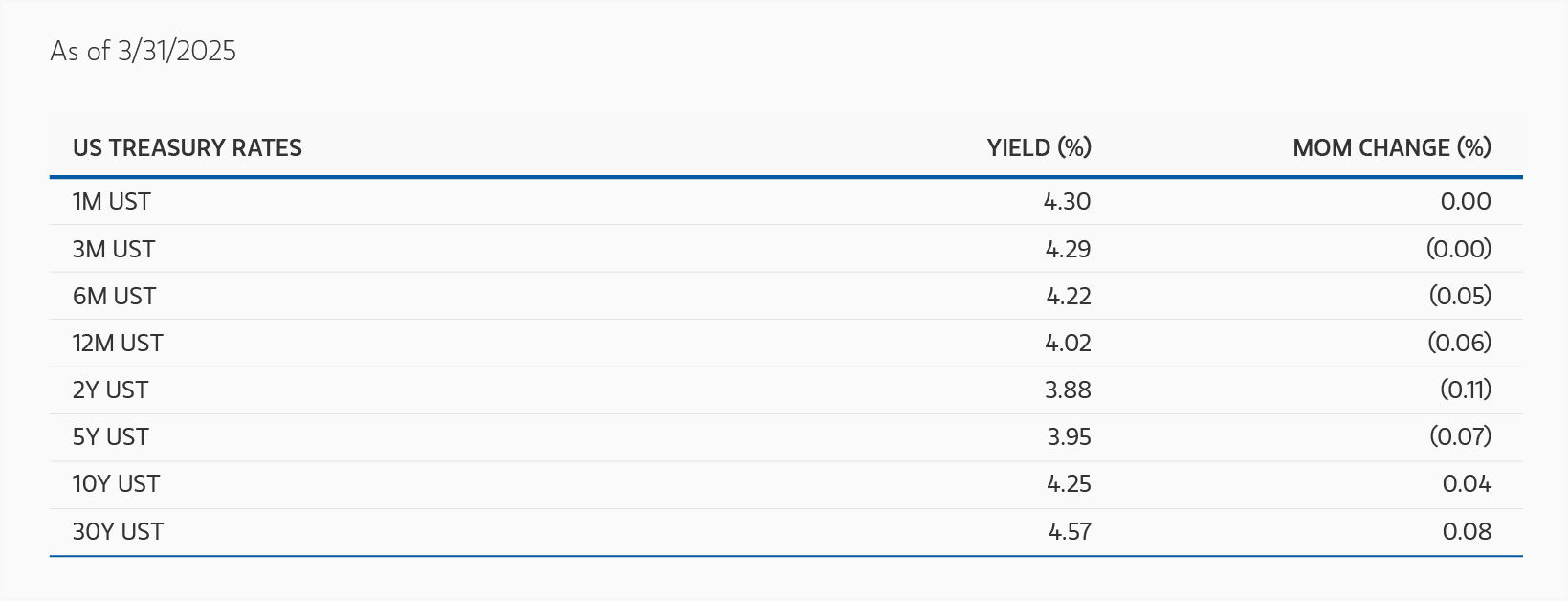

Monthly Interest Rate Summary as of 3/31/25.

Monthly Interest Rate Summary as of 3/31/25.

DISPLAY 1

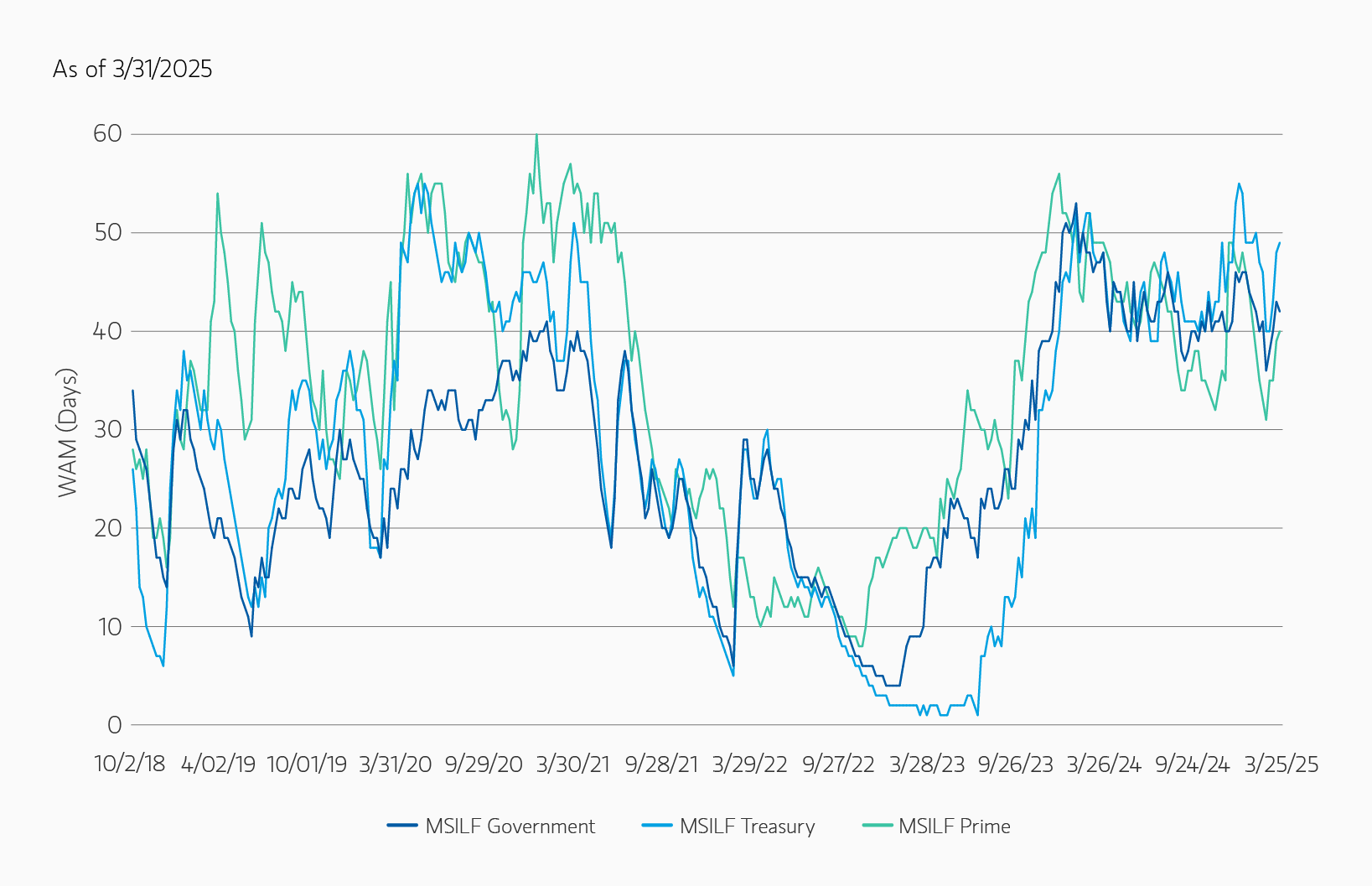

MSILF Weighted Average Maturities (WAM) Summary as of 3/31/25.2

MSILF Weighted Average Maturities (WAM) Summary as of 3/31/25.2

DISPLAY 2

PORTFOLIO STRATEGY

Government/Treasury Strategy

We continue to hold attractive positions in both fixed- and floating-rate securities as the money market curve is still flat. Tailwinds for SOFR (secured overnight financing rate) remained, especially around quarter-end, causing overnight and short-term floating-rate positions to be attractive. The level of uncertainty in the market has grown dramatically through the month, with a wide range of near-term outcomes for markets. As such we have maintained the portfolios’ weighted average maturity (WAM) in the mid- to low-40 days, with fixed-rate positioning that we believe is likely to perform well if the rate-cutting cycle continues through the midpoint of this year.

The market closed the month pricing roughly three rate cuts for 2025, one more than the two predicted in the Fed’s most recent dot plot. The pricing of the additional cut is likely related to growth concerns on the back of political initiatives, with many market-wide gross domestic product (GDP) measures and estimates being revised downward in the absence of further clarity on tariffs. The Fed, however, has conveyed a willingness to be patient while still seeming to indicate that the path of least resistance will be toward rate cuts, especially if officials gain further confidence on the inflation front or see weakening in labor markets.

The debt ceiling “X-date” is approaching, and tax receipts through the first half of April will be worth watching. Treasury bill auction sizes have fallen, and the potential for more ad-hoc cash management bills in the near future is rising. Market participants will need to be very diligent on the concentration of specific bonds they own as more formal information relating to the debt ceiling arises.

Prime Strategy3

Both the WAM and weighted average life (WAL) of the portfolios extended throughout the month as we took advantage of the recent sell-off in the short end of the curve and opportunistically locked in 1-year fixed-rate securities with a positive carry compared to overnight repo securities.

With credit spreads returning to a more normalized level following the year-end turn, we believe secondary market rolled-down corporate bonds continue to provide the most value and are trading dislocated, priced cheaply relative to their wholesale equivalents. We looked to add exposure mostly around month-end during index selling.

From a liquidity standpoint, dealer balance sheets remain unconstrained, which is one of the main reasons for the spread tightening in the first quarter of the year.

Featured Insights