At year-end, investors often review portfolios, rebalance allocations and plan for taxes. This is also a good time to update adjusted gross income (AGI) projections and assess how charitable giving fits into overall financial goals. By incorporating tax management into planned giving, you can help clients achieve their philanthropic goals while also maximizing potential tax benefits.

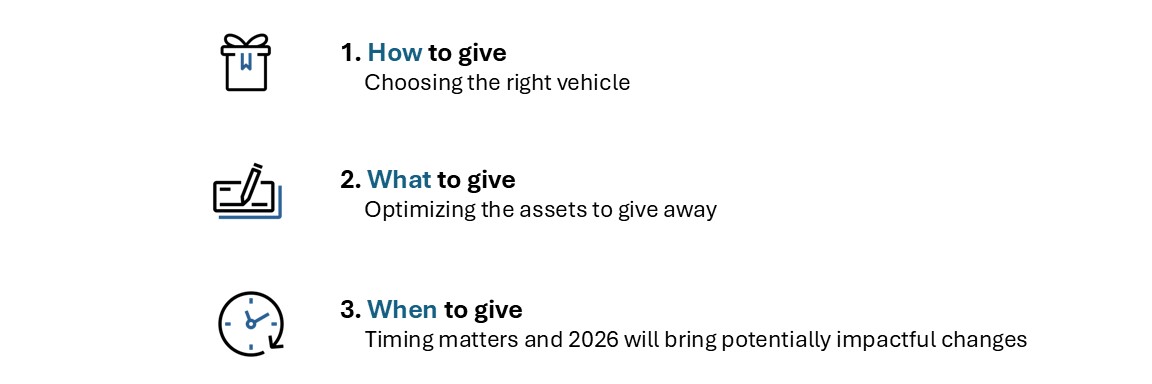

There are three main factors to discuss with clients considering charitable giving, each impacting potential tax results and long-term effectiveness:

Let’s take a moment to unpack each consideration:

How to give:

- Direct gifts are outright gifts to qualified charities. They’re simple and can provide an upfront deduction (up to applicable AGI limits).

- Donor-advised funds allow you to make a deductible gift today while distributing funds to charities over time.

- Charitable trusts, such as charitable remainder trusts, can provide income to you or your beneficiaries while reserving a future benefit for charitable organizations.

- Pooled income funds can offer a turnkey alternative to charitable trusts with potential advantages such as a higher deduction and tax-preferential income.

What to give:

- Cash, like writing a check, offers simplicity and the deductibility limit is generally up to 60% of AGI. However, it can often be advantageous to keep your cash on hand and consider the potential tax benefits of gifting appreciated assets.

- Appreciated securities, such as stocks or mutual fund shares held for more than one year, are often among the most efficient assets to give away. Donating them directly to charity may allow you to avoid capital gains recognition while deducting the fair market value of the gift. The deductibility limit for appreciated assets is generally up to 30% of AGI.

- Private business interests, real estate, or other non-cash assets can also be contributed in certain cases. Though these may require additional due diligence and valuation.

- Qualified charitable distributions from IRAs remain an effective tool for investors aged 70½ or older to reduce taxable income while satisfying required minimum distributions.

When to give:

For top-bracket clients, claiming charitable or itemized deductions in 2025 may be more advantageous than in 2026 due to the One Big Beautiful Bill Act passed earlier this year. Below are two key provisions affecting itemized charitable deductions.

- 1. Itemized deductions limited to 35% for top tax rates - Starting in 2026, individuals subject to the highest marginal tax rate (37%) will see their itemized deductions capped at 35%. For example, a $100,000 charitable gift would yield $37,000 in tax savings in 2025, but only $35,000 in 2026.

- 2. 0.5% floor on charitable deductions - A new 0.5% AGI floor will apply to charitable deductions for itemizers, before the standard AGI limits. For example, a donor with $1,000,000 AGI may only deduct contributions exceeding $5,000. A $100,000 gift of appreciated assets would be reduced to $95,000, subject to the 30% AGI limit.

Bottom line: Charitable giving is both a personal and financial commitment. Use year-end as an opportunity to review your clients’ AGI projections, portfolio compositions and philanthropic goals to ensure their giving strategies support their causes and financial plans.

Register for our Continuing Education (CE) Course: Wealth to Legacy: Guiding Clients Through Tax-Smart Philanthropy to understand how clients may be able to align charitable intent with desired financial planning outcomes and more.