In August, we shared our view that the municipal bond yield curve was signaling a rare opportunity for investors. In this blog, we outline why we believe there is still a compelling case for investing at the long end of the municipal yield curve.

The opportunity stems from the performance of long-term municipal bonds, which year-to-date has significantly lagged not only the short-term portion of the municipal curve, but the broader domestic bond market as well. Long-term munis have had a total return of 0.31%1 through Sept. 30, compared with 4.51%2 for the 5-year maturity municipals and 6.88%3 for investment-grade corporate bonds (see index definitions below). Weaker performance has kept long-term muni yields attractive, while surging demand for short-term munis has boosted prices and lowered yields.

Steep and Cheap

As a result, we believe the municipal curve merits the label of “steep and cheap.” Cheap, because long- term munis yielded 4.63%1 on Sept. 30, vs. the 10-year average of 3.28%, and not too far behind the taxable yield on investment-grade corporates of 4.81%.3 For perspective, investors in the highest federal tax bracket of 40.8% would need to find a taxable bond yielding 7.82% (known as the tax equivalent yield4) to match the after-tax 4.63% of long-end munis.

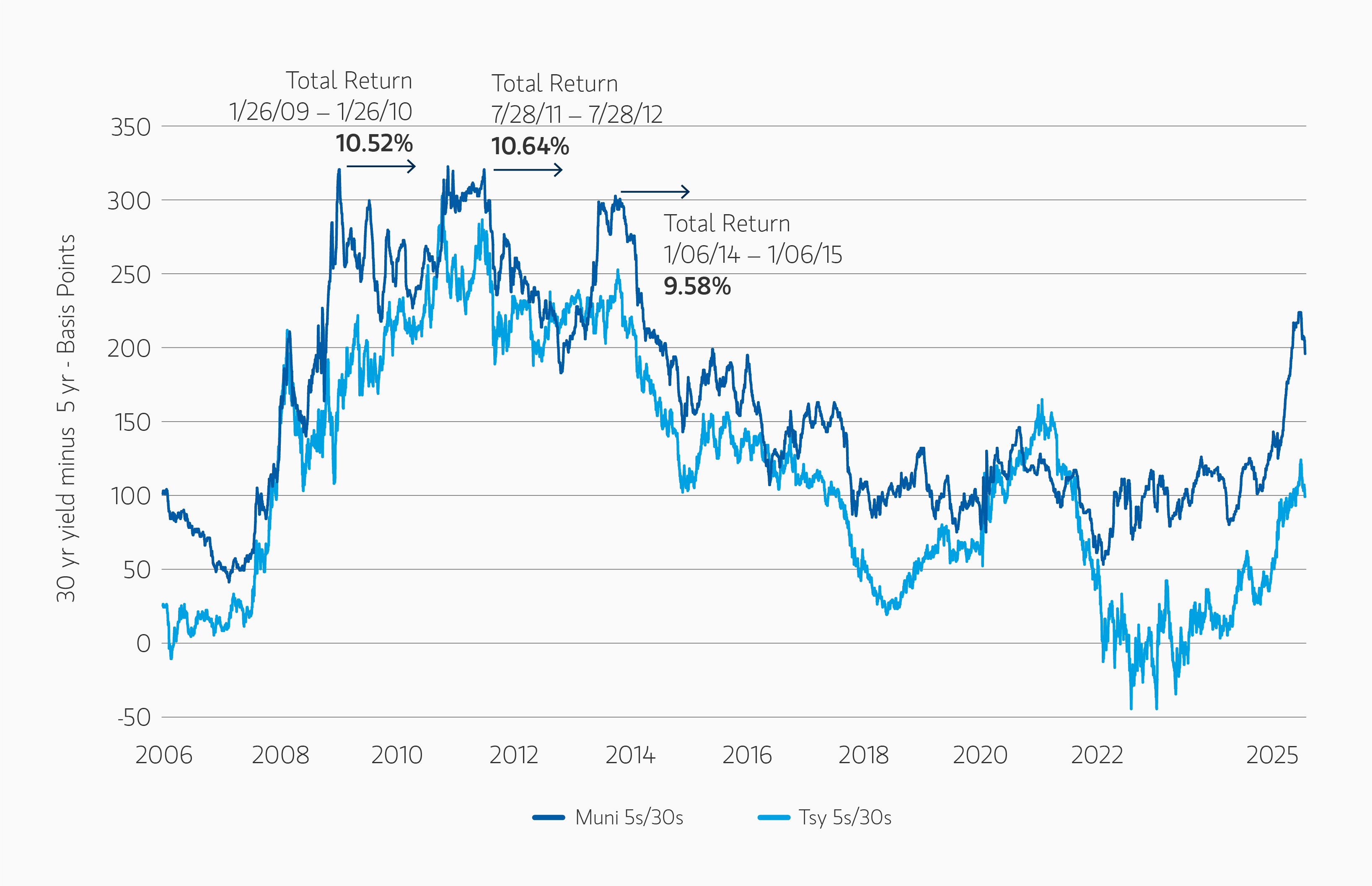

But the attractive starting yield in today’s muni market is just half the story. In the past two decades, municipal yield curves of this steepness have been predictors of attractive total returns going forward. Steepness is measured as the difference in yields between the 30-year5 and 5-year2 benchmark municipal yields.

Consider three steep yield curve episodes since 2006: the Global Financial Crisis (GFC) of 2007 to 2008, the Meredith Whitney scare of 2010 to 2011,6 and the 2013 Taper Tantrum.7 Exhibit 1 illustrates the total returns for the 12-month periods following the three peaks: 10.52%, 10.64% and 9.58%,5 respectively.

Steep yield curves have been predictors of strong returns in the following 12 mos.

Steep yield curves have been predictors of strong returns in the following 12 mos.

Exhibit 1

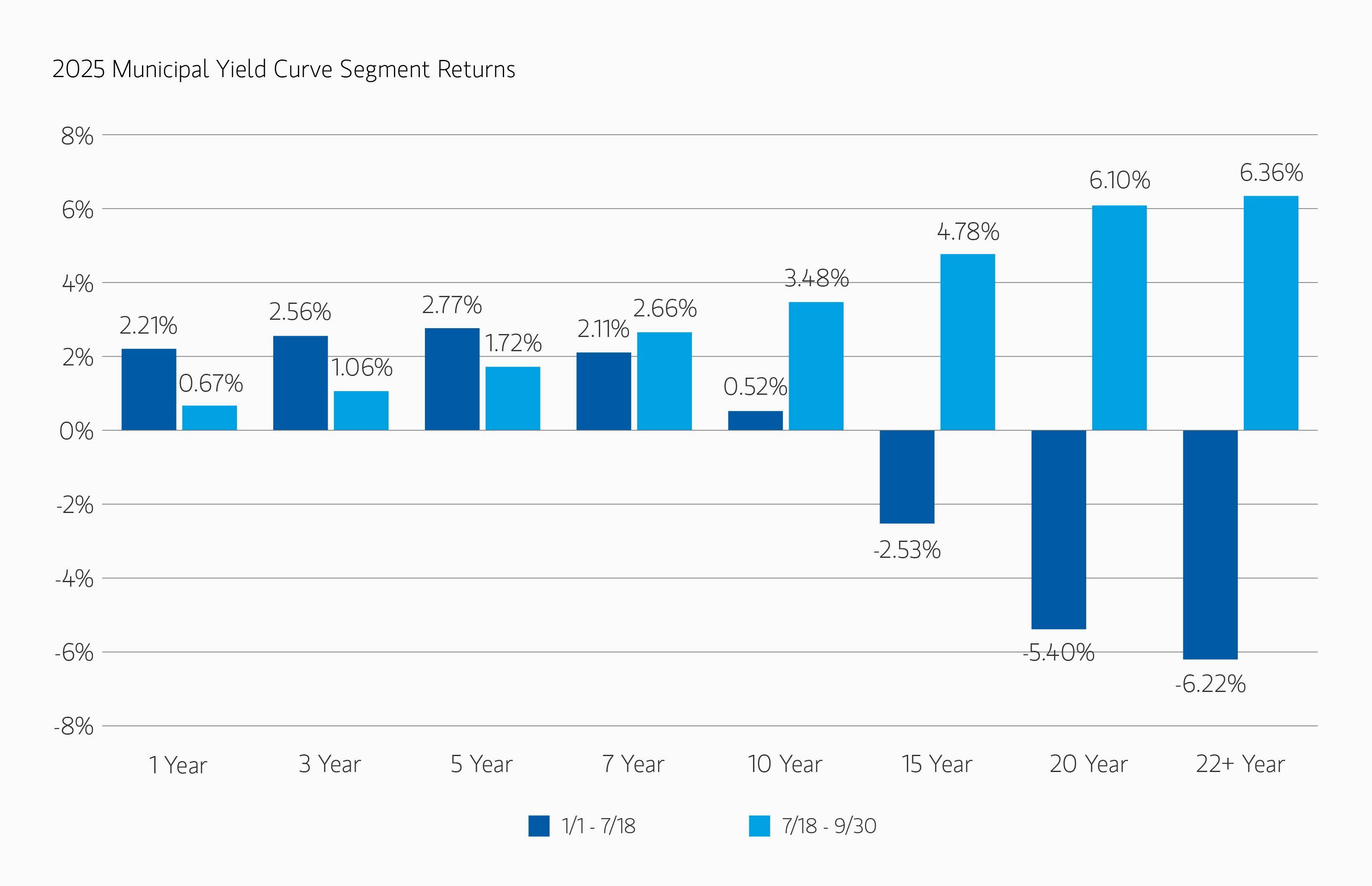

A marked turnaround for long-term munis

What explains the strong performance following steep yield curve episodes? When the long end of the curve significantly underperforms short and intermediate sectors, investors start to view it as a value opportunity, and their buying boosts prices, which works to flatten the curve to a more typical relationship.

Indeed, since we published our blog in August about value at the long end of the curve, a marked turnaround for long-term munis has begun to occur. Losses hit bottom on July 18, and since then through Sept. 30, the 22+ year maturity has returned 6.36%1, after losing 6.22% for the year up to that date (Exhibit 2), recouping the loss for the first part of the year. The 20-, 15- and 10-year sectors8 showed similar turnarounds, while the short end showed markedly lower relative performance during the same time period.

Now underway: A big turnaround in long-term munis.

Now underway: A big turnaround in long-term munis.

Exhibit 2

We see room to run for long-term munis

Despite the incipient turnaround in long-term muni bonds, we still believe this represents a rare opportunity for investors. While the spread between the municipal long end (30 years)5 vs. short (5 years)2 has narrowed from its widest point in August by 22 bps to 192 bps, the spread is still the greatest it has been since 2014 (Exhibit 1), and significantly higher than the average of 160 bps since 2006.

Moreover, the technical factors behind the weakness in long-term munis appear to be diminishing. Supply surged in the first half of the year, in large part driven by uncertainty over the “One Big Beautiful Bill” Act, which raised the possibility of changes to the municipal bond tax exemption. Issuers raced to get ahead of that possibility, while investors’ appetite for that paper could not fully keep up with new supply. The accelerated pace of issuance in the first half of 2025 also stemmed from rising infrastructure and capital project costs, and the need to fill budget gaps left by depleted COVID-19-era funding.

As issuance pressure and macro uncertainty have subsided, long-term bond investors have returned to the scene. For example, flows into long-term municipal bond ETFs, which turned negative in April, began picking up again in July, and reached $9.6 billion for the year in September (Source: Refinitiv).

Bottom Line: Historically, a steep municipal curve has signaled strong forward returns. Such opportunities rarely persist without drawing investor interest, and we have witnessed that in dramatic fashion since July. But we believe that technical and fundamental forces are still bullish for long-term munis; it is an excellent occasion for investors to consider starting or adding to their allocation to the sector.

Featured Insights