We enter the second quarter of 2026 with a constructive view on securitized credit, even as spreads have widened across both agency and non-agency sectors in recent months. Rather than signaling a deterioration in fundamentals, we view this widening as primarily macro-driven—reflecting broader risk repricing tied to geopolitical uncertainty, oil price volatility and elevated issuance in corporate credit markets, particularly associated with ongoing AI-related capital expenditure. In our view, this repricing has created more attractive entry points across securitized markets rather than weakening the underlying investment case.

Importantly, securitized credit remains relatively insulated from many of these forces. Unlike corporate credit, which is more directly exposed to cyclical earnings risk, input cost pressures (including energy), and heavy primary issuance linked to AI infrastructure investment, securitized assets are predominantly backed by pools of loans tied to the real economy—especially housing and high-quality consumer balance sheets. While there are pockets of exposure, such as data centers, aircraft and autos, these represent a relatively small portion of the broader securitized universe.

Instead, the sector’s performance is more closely linked to household balance sheets—particularly higher-income consumers, who continue to exhibit strong credit performance supported by substantial home equity and financial asset appreciation over the past several years. This high-end consumer exposure remains a key differentiator, as it has helped support stable credit performance even amid a more uncertain macro backdrop.

As a result, securitized credit today offers a compelling combination: the ability to generate high yield–like income, with yields approaching ~6%, alongside average credit quality in the A/A+ range, backed by hard, income-generating assets. At the same time, the asset class has historically exhibited lower volatility, as well as less frequent and less severe drawdowns, than comparably yielding corporate credit.

Against this backdrop, we believe securitized markets—and in particular diversified strategies such as the MS INVF Global Asset-Backed Securities Fund—represent one of the most attractive relative value opportunities in fixed income today. Should spreads continue to widen and valuations become even more compelling, we would expect to further increase allocations to the asset class.

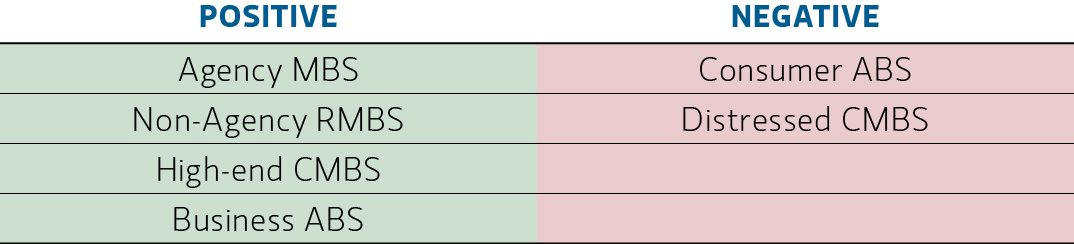

Securitized Highest Conviction Trades

Securitized Highest Conviction Trades

Display 1

Agency MBS

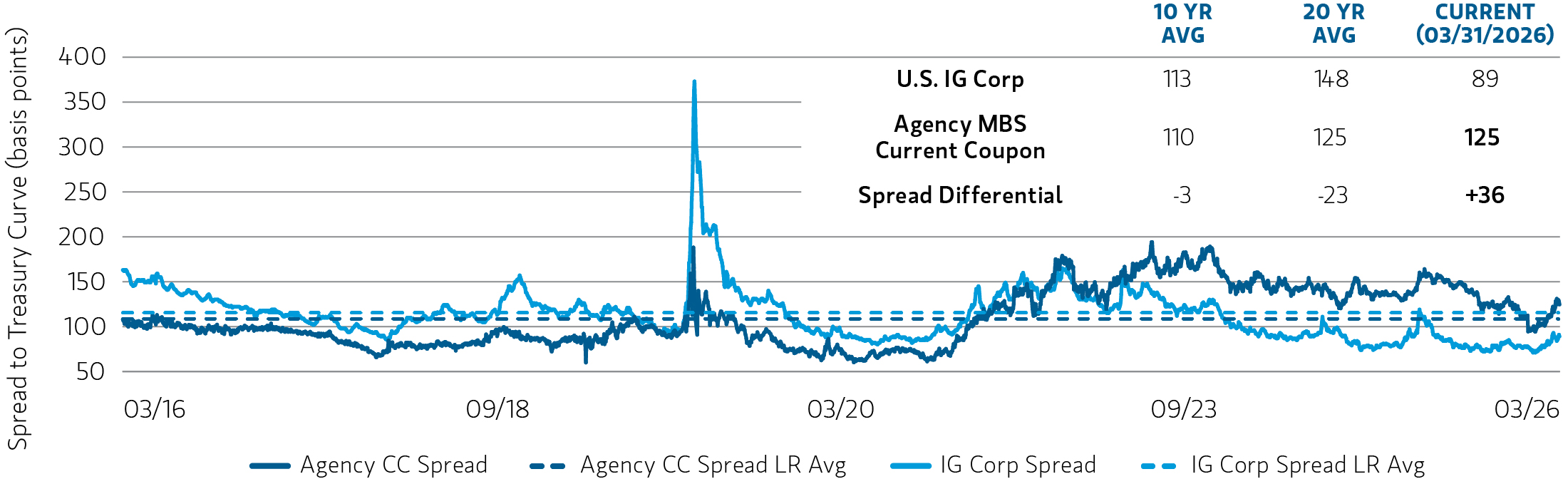

We began 2026 with a positive outlook for agency mortgage-backed securities (MBS), and that view remains intact even as spreads have widened modestly alongside broader fixed income markets. The recent widening reflects macro risk sentiment rather than any deterioration in underlying fundamentals, and in our view has improved the relative value opportunity.

Agency MBS continues to offer attractive risk-adjusted valuations versus other fixed income sectors, particularly corporate bonds, which face ongoing supply pressure from elevated issuance. In contrast, agency MBS benefits from a more stable and diversified demand base and remains relatively insulated from corporate leverage cycles and AI-driven capex trends.

Following the tightening observed in January after policy support for GSE purchases, spreads have partially retraced. However, current coupon agency MBS still offers yields in the ~5% range, which remains compelling for a high-quality, government-backed asset class.

We expect long-maturity U.S. rates to remain elevated in 2026, with the 10-year Treasury yield near 4%. This should keep mortgage rates high, limiting refinancing activity and prepayment risk, and thereby supporting carry and income generation.

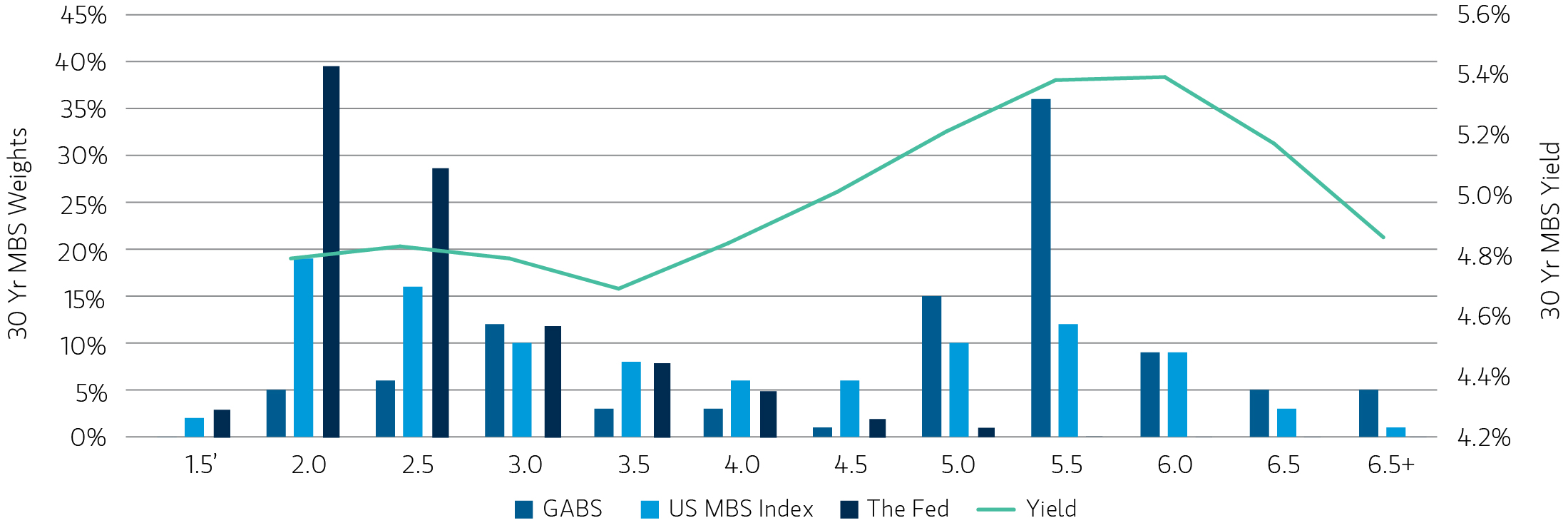

We remain positioned with an overweight to current coupon 30-year MBS in order to maximize income and carry, while maintaining less exposure to 15-year and lower coupon 30-year MBS where carry is less compelling. In terms of structure, we favor specified pools and CMOs, where prepayment risk can be more effectively managed through favorable loan characteristics and structural protections.

From a technical perspective, supply-demand dynamics remain favorable. While gross supply, including Fed runoff, is expected to remain elevated, we anticipate that it will be well absorbed by GSEs, banks, money managers, REITs and foreign investors. A potential rate-cutting cycle could further support bank demand for MBS.

Agency MBS Cheap Versus U.S. Corporates

Agency MBS Cheap Versus U.S. Corporates

Display 2

Maximize Yield in Current Coupon MBS

Maximize Yield in Current Coupon MBS

Display 3

Residential Credit (Non-Agency RMBS)

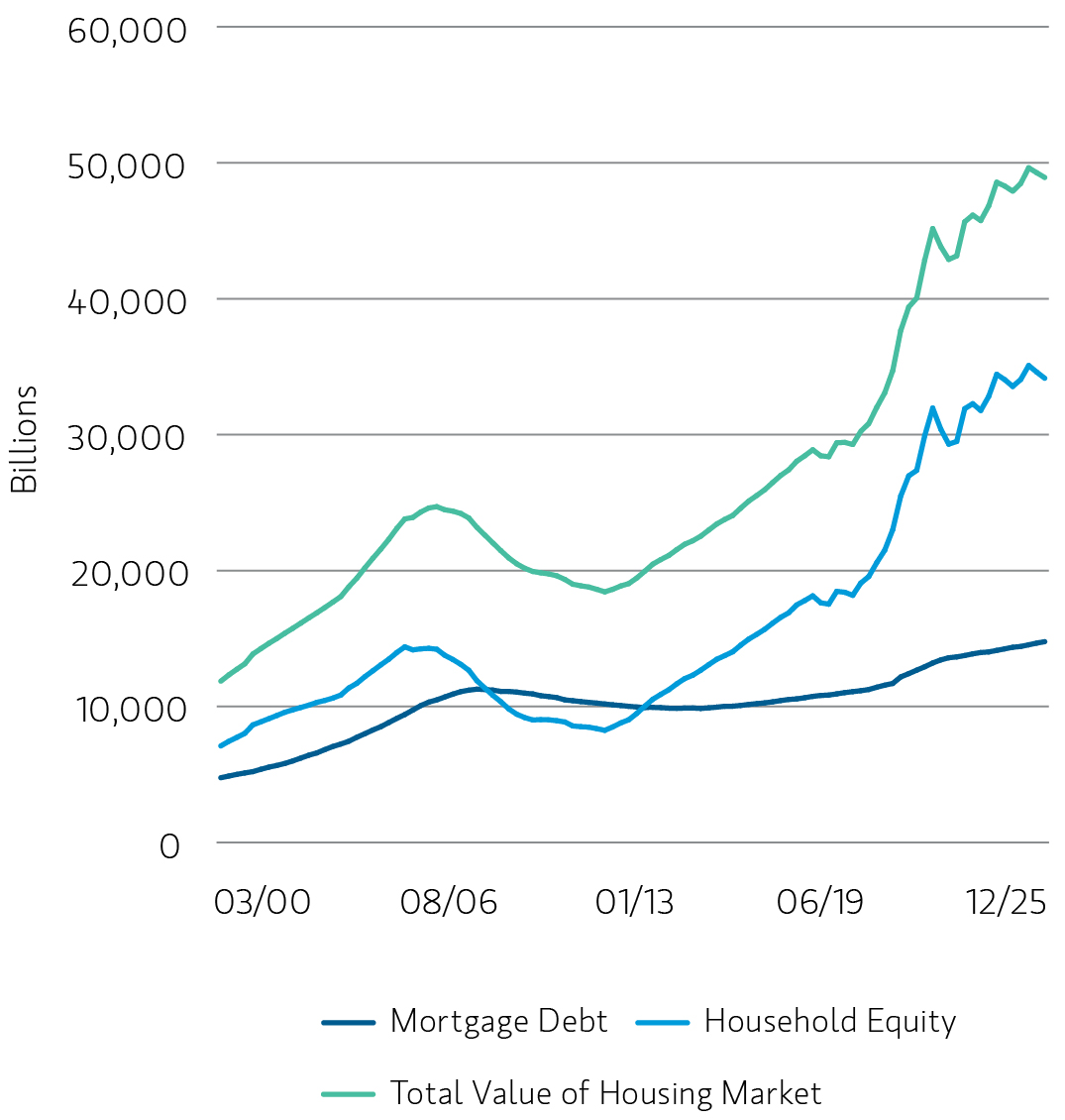

Non-agency RMBS remains our highest-conviction sector within securitized credit. Despite recent spread widening, fundamentals remain exceptionally strong, and valuations have become more compelling.

This sector is particularly well insulated from broader macro risks such as geopolitical shocks or commodity price volatility. Instead, performance is driven by the strength of household balance sheets, especially among higher-income borrowers, which continue to benefit from significant accumulated housing equity and financial wealth.

Record levels of homeowner equity, supported by several years of home price appreciation, have resulted in average loan-to-value ratios below 50%, providing meaningful loss protection even under stress scenarios. At the same time, delinquency and default rates remain at historically low levels.

We expect home prices to remain broadly stable in 2026, following modest 1–2% appreciation in 2025. While affordability remains a challenge, limited housing supply and strong demographic demand should continue to support the market.

Mortgage credit performance remains pristine, and we expect this trend to continue. Similar dynamics are evident in parts of the UK and Europe, where strong equity cushions, limited supply and low arrears provide additional support.

In our view, residential credit remains one of the most attractive ways to take credit risk globally, offering high income potential with strong structural protection and limited sensitivity to broader macro shocks.

Historic Levels of Home Equity from HPA

Historic Levels of Home Equity from HPA

Display 4

Commercial Mortgage (CMBS): Fundamentals improving after a multi-year reset

After several years of headwinds driven by higher rates and post-pandemic dislocations, CMBS fundamentals are improving. While spreads have widened alongside broader markets, underlying property-level performance is stabilizing.

Vacancy rates that surged during the pandemic are trending back toward pre-pandemic levels in many markets, while subdued new construction activity has improved the supply-demand balance across several property types. Financing conditions have also stabilized relative to prior periods of stress.

The CMBS market remains highly idiosyncratic, and we maintain a strong quality bias within each subsector.:

- Hotels: luxury leisure properties over economy or business-oriented hotels

- Multifamily: higher-quality, well-located apartments over affordable housing units

- Retail: high-income, destination-oriented malls over lower-end discount centers

- Office: “trophy” and Class A assets over commodity Class B/C buildings

After several years of reducing exposure, we are looking to selectively increase CMBS allocations in 2026, focusing on structures and collateral where we believe the margin of safety is most attractive.

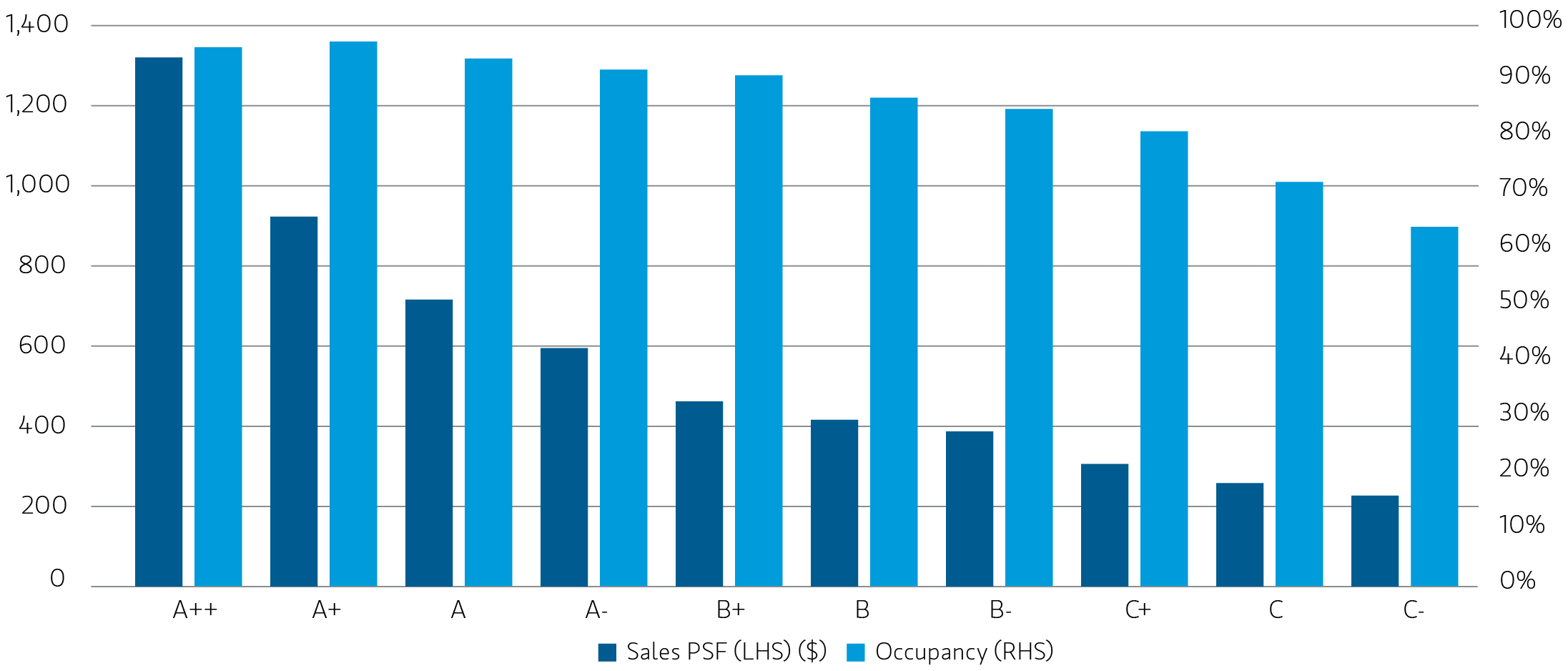

Retail: High-End Shopping Centers Performing Well

Retail: High-End Shopping Centers Performing Well

Display 5

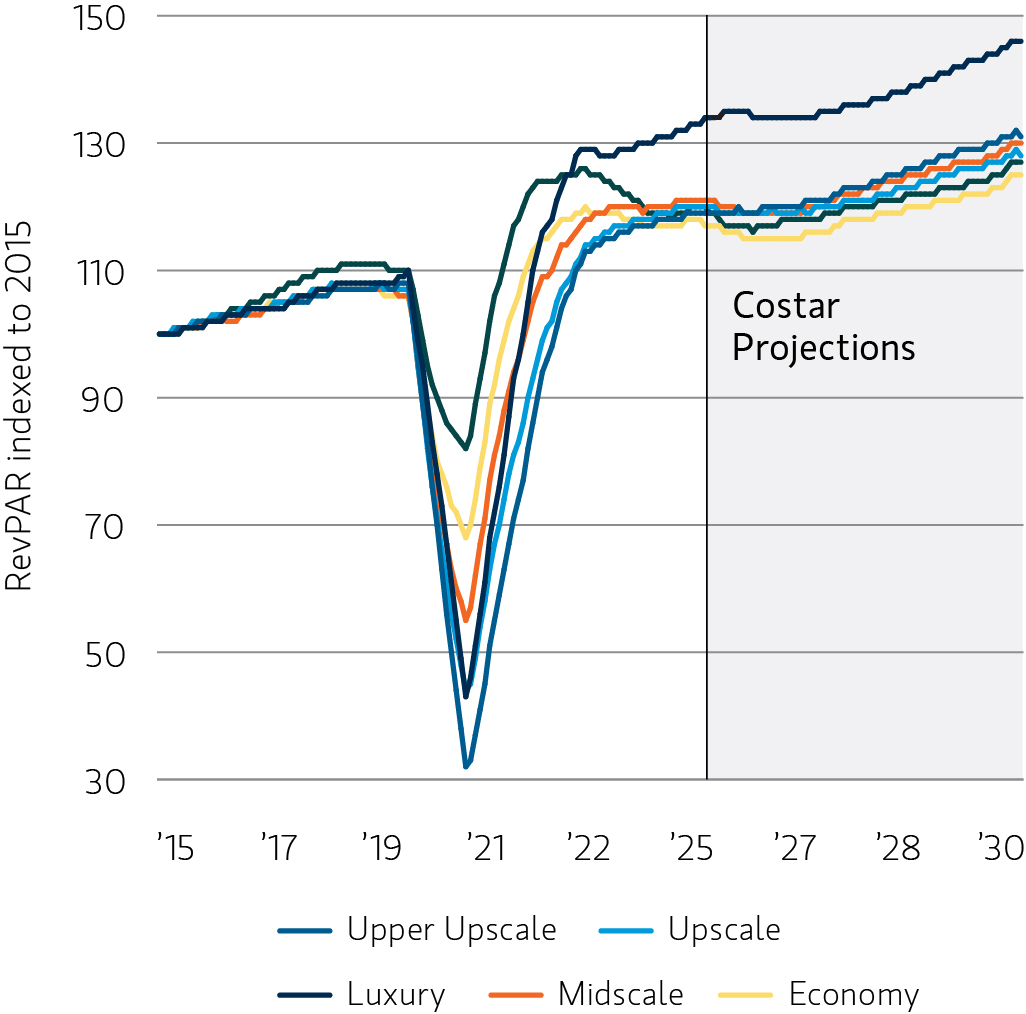

Luxury Hotels Performing Well

Source: Costar, STR., MSIM, as of 9/30/2026

Luxury Hotels Performing Well

Display 6

Asset Backed Markets (ABS): Selective, with a tilt to business-oriented collateral

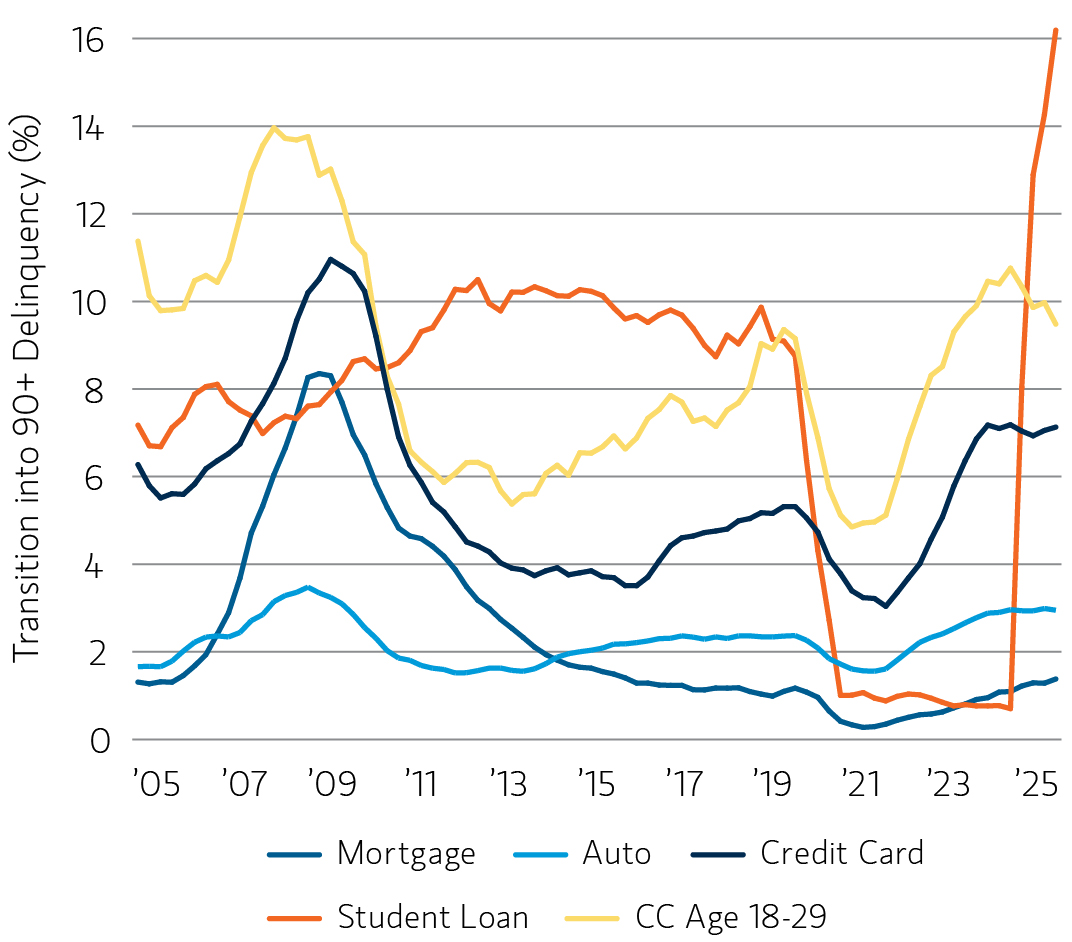

Our overall positioning in ABS remains selective. While spread widening has improved relative value in some segments, fundamental divergence persists across consumer cohorts.

Lower-income consumers continue to face pressure from elevated inflation and higher borrowing costs, with delinquency and default rates rising in non-prime segments. In contrast, higher-income consumers remain resilient, supported by accumulated wealth from both housing and financial assets.

As a result, we emphasize higher-quality consumer exposure and favor business-oriented ABS, where fundamentals tend to be more stable and less sensitive to consumer stress. Areas of focus include aircraft leasing, data centers, mortgage servicing rights and small business loans.

While certain subsectors have some linkage to broader macro themes, such as data centers and AI infrastructure, overall exposure remains limited, and the securitized market as a whole remains far less sensitive to these dynamics than corporate credit.

Consumer ABS Under Stress, Mortgage Delinquencies Remain Low Post GFC

Consumer ABS Under Stress, Mortgage Delinquencies Remain Low Post GFC

Display 7

Conclusion

We believe securitized credit remains one of the most compelling opportunities in fixed income today, particularly in an environment characterized by geopolitical uncertainty, oil price volatility and elevated corporate issuance tied to AI investment.

In contrast to corporate credit, securitized assets are less exposed to geopolitical and commodity-driven earnings risk, relatively insulated from AI-driven issuance and capex cycles, and primarily tied to high-quality household balance sheets and real assets.

This results in a unique investment profile: the ability to generate high yield–like income, with yields around ~6%, while maintaining average credit quality in the A/A+ range, backed by physical collateral. At the same time, the asset class has historically exhibited lower volatility, as well as less frequent and less severe drawdowns, than similarly yielding alternatives.

Additionally, the recent widening in spreads across securitized markets has further enhanced relative value. If this trend continues, we would expect to increase allocations to securitized credit, where we see the most attractive risk-adjusted opportunities.

Against this backdrop, we believe strategies such as the MS INVF Global Asset-Backed Securities Fund are particularly well positioned. With diversified exposure across agency and non-agency sectors, a focus on higher-quality collateral and disciplined structural risk management, the strategy offers an efficient way to access the attractive income, resilience and diversification benefits that securitized credit provides today.

In our view, for investors seeking a combination of income, quality and stability in an uncertain macro environment, securitized credit—and this strategy in particular—stands out as one of the most attractive relative value opportunities available.

Featured Insights

RISK CONSIDERATIONS

Treasury bonds are backed by the full faith and credit of the US government if held to maturity. Not all government agency bonds are backed by the full faith and credit of the US government. It is possible that these issuers will not have the funds to meet their payment obligations in the future. Fixed income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest-rate risk), the creditworthiness of the issuer and general market liquidity (market risk). In a rising interest-rate environment, bond prices may fall and may result in periods of volatility and increased portfolio redemptions. In a declining interest-rate environment, the portfolio may generate less income. Longer-term securities may be more sensitive to interest rate changes. Mortgage and asset-backed securities are sensitive to early prepayment risk and a higher risk of default and may be hard to value and difficult to sell (liquidity risk). They are also subject to credit, market and interest-rate risks. Active management attempts to outperform a passive benchmark through proactive security selection and assumes considerable risk should managers incorrectly anticipate changing conditions.

DEFINITION

A basis point is a unit of measure, equal to one hundredth of a percentage point, used in finance to describe the percentage change in the value or rate of a financial instrument.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”) and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial, and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results.

The indexes are unmanaged and do not include any expenses, fees, or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold, or promoted by the applicable licensor and it shall not have any liability with respect thereto.

This material is not a product of Morgan Stanley’s Research Department and should not be regarded as a research material or a recommendation.

The Firm has not authorized financial intermediaries to use and to distribute this material unless such use and distribution is made in accordance with applicable law and regulation. Additionally, financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide this material in view of that person’s circumstances and purpose. The Firm shall not be liable for, and accepts no liability for, the use or misuse of this material by any such financial intermediary.

This material may be translated into other languages. Where such a translation is made this English version remains definitive. If there are any discrepancies between the English version and any version of this material in another language, the English version shall prevail.

The whole or any part of this material may not be directly or indirectly reproduced, copied, modified, used to create a derivative work, performed, displayed, published, posted, licensed, framed, distributed, or transmitted or any of its contents disclosed to third parties without the Firm’s express written consent. This material may not be linked to unless such hyperlink is for personal and non-commercial use. All information contained herein is proprietary and is protected under copyright and other applicable law.

Eaton Vance is part of Morgan Stanley Investment Management. Morgan Stanley Investment Management is the asset management division of Morgan Stanley.

DISTRIBUTION

This material is only intended for and will only be distributed to persons resident in jurisdictions where such distribution or availability would not be contrary to local laws or regulations.

MSIM, the asset management division of Morgan Stanley (NYSE: MS), and its affiliates have arrangements in place to market each other’s products and services. Each MSIM affiliate is regulated as appropriate in the jurisdiction it operates. MSIM’s affiliates are: Eaton Vance Management (International) Limited, Eaton Vance Advisers International Ltd, Calvert Research and Management, Eaton Vance Management, Parametric Portfolio Associates LLC, Parametric SAS and Atlanta Capital Management LLC.

This material has been issued by any one or more of the following entities:

EMEA:

In the EU, MSIM materials are issued by MSIM Fund Management (Ireland) Limited (“FMIL”). FMIL is regulated by the Central Bank of Ireland and is incorporated in Ireland as a private company limited by shares with company registration number 616661 and has its registered address at 24-26 City Quay, Dublin 2, DO2 NY19, Ireland.

Outside the EU, MSIM materials are issued by Morgan Stanley Investment Management Limited (MSIM Ltd) is authorised and regulated by the Financial Conduct Authority. Registered in England. Registered No. 1981121. Registered Office: 25 Cabot Square, Canary Wharf, London E14 4QA.

In Switzerland, MSIM materials are issued by Morgan Stanley & Co. International plc, London (Zurich Branch) Authorised and regulated by the Eidgenössische Finanzmarktaufsicht ("FINMA"). Registered Office: Beethovenstrasse 33, 8002 Zurich, Switzerland.

Italy: MSIM FMIL (Milan Branch), (Sede Secondaria di Milano) Palazzo Serbelloni Corso Venezia, 16 20121 Milano, Italy. The Netherlands: MSIM FMIL (Amsterdam Branch), Rembrandt Tower, 11th Floor Amstelplein 1 1096HA, Netherlands. France: MSIM FMIL (Paris Branch), 61 rue de Monceau 75008 Paris, France. Spain: MSIM FMIL (Madrid Branch), Calle Serrano 55, 28006, Madrid, Spain. Germany: MSIM FMIL Frankfurt Branch, Große Gallusstraße 18, 60312 Frankfurt am Main, Germany (Gattung: Zweigniederlassung (FDI) gem. § 53b KWG). Denmark: MSIM FMIL (Copenhagen Branch), Gorrissen Federspiel, Axel Towers, Axeltorv2, 1609 Copenhagen V, Denmark.

MIDDLE EAST

Dubai International Financial Centre: This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE (including the Dubai International Financial Centre and the Abu Dhabi Global Market) and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or government agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Abu Dhabi Global Market ("ADGM"): This material is sent strictly within the context of, and constitutes, an Exempt Communication. This material relates to (strategy) which is not subject to any form of regulation or approval by the Financial Services Regulatory Authority of the Abu Dhabi Global Market (the “FSRA”).

Saudi Arabia

This financial promotion was issued and approved for use in Saudi Arabia by Morgan Stanley Saudi Arabia, Al Rashid Tower, Kings Sand Street, Riyadh, Saudi Arabia, authorized and regulated by the Capital Market Authority license number 06044-37.

US

NOT FDIC INSURED | OFFER NO BANK GUARANTEE | MAY LOSE VALUE | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT A DEPOSIT

Latin America (Brazil, Chile Colombia, Mexico, Peru, and Uruguay)

This material is for use with an institutional investor or a qualified investor only. All information contained herein is confidential and is for the exclusive use and review of the intended addressee and may not be passed on to any third party. This material is provided for informational purposes only and does not constitute a public offering, solicitation, or recommendation to buy or sell for any product, service, security and/or strategy. A decision to invest should only be made after reading the strategy documentation and conducting in-depth and independent due diligence.

ASIA PACIFIC

Hong Kong: This document has been issued by Morgan Stanley Asia Limited, CE No. AAD291, for use in Hong Kong and shall only be made available to “professional investors” as defined under the Securities and Futures Ordinance of Hong Kong (Cap 571). The contents of this document have not been reviewed nor approved by any regulatory authority including the Securities and Futures Commission in Hong Kong. Accordingly, save where an exemption is available under the relevant law, this document shall not be issued, circulated, distributed, directed at, or made available to, the public in Hong Kong. Singapore[ This material is disseminated in Singapore by Morgan Stanley Investment Management Company, Registration No. 199002743C. This material should not be considered to be the subject of an invitation for subscription or purchase, whether directly or indirectly, to the public or any member of the public in Singapore other than (i) to an institutional investor under section 304 of the Securities and Futures Act, Chapter 289 of Singapore (“SFA”), (ii) to a “relevant person” (which includes an accredited investor) pursuant to section 305 of the SFA, and such distribution is in accordance with the conditions specified in section 305 of the SFA; or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. This material has not been reviewed by the Monetary Authority of Singapore. Australia: This material is provided by Morgan Stanley Investment Management (Australia) Pty Ltd ABN 22122040037, AFSL No. 314182 and its affiliates and does not constitute an offer of interests. Morgan Stanley Investment Management (Australia) Pty Limited arranges for MSIM affiliates to provide financial services to Australian wholesale clients. This material will not be lodged with the Australian Securities and Investments Commission.

Japan: For professional investors, this material is circulated or distributed for informational purposes only. For those who are not professional investors, this material is provided in relation to Morgan Stanley Investment Management (Japan) Co., Ltd. (“MSIMJ”)’s business with respect to discretionary investment management agreements (“IMA”) and investment advisory agreements (“IAA”). This is not for the purpose of a recommendation or solicitation of transactions or offers any particular financial instruments. Under an IMA, with respect to management of assets of a client, the client prescribes basic management policies in advance and commissions MSIMJ to make all investment decisions based on an analysis of the value, etc. of the securities, and MSIMJ accepts such commission. The client shall delegate to MSIMJ the authorities necessary for making investment. MSIMJ exercises the delegated authorities based on investment decisions of MSIMJ, and the client shall not make individual instructions. All investment profits and losses belong to the clients; principal is not guaranteed. Please consider the investment objectives and nature of risks before investing. As an investment advisory fee for an IAA or an IMA, the amount of assets subject to the contract multiplied by a certain rate (the upper limit is 2.20% per annum (including tax)) shall be incurred in proportion to the contract period. For some strategies, a contingency fee may be incurred in addition to the fee mentioned above. Indirect charges also may be incurred, such as brokerage commissions for incorporated securities. Since these charges and expenses are different depending on a contract and other factors, MSIMJ cannot present the rates, upper limits, etc. in advance. All clients should read the Documents Provided Prior to the Conclusion of a Contract carefully before executing an agreement. This material is disseminated in Japan by MSIMJ, Registered No. 410 (Director of Kanto Local Finance Bureau (Financial Instruments Firms)), Membership: the Japan Securities Dealers Association, The Investment Trusts Association, Japan, the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association.