Monthly Review

April saw a partial reversal of March’s risk-off move across global fixed income and credit markets as volatility eased following a temporary ceasefire between the U.S. and Iran. Although geopolitical tensions remained elevated and energy markets continued to reflect a meaningful risk premium, reduced tail risks supported an improvement in broader market sentiment. The month was characterized by a stabilization in credit conditions, a retracement in spreads, and a reassessment of the more aggressive inflation and policy repricing that dominated March.

Energy remained the primary macro transmission channel. While disruption risk around the Strait of Hormuz and broader Middle East tensions kept oil prices elevated, markets increasingly focused on the likelihood that supply disruptions would remain contained.

Rates markets remained volatile but more orderly relative to March. Treasury yields moved modestly higher, with the U.S. 10-year ending April near 4.37% and the German 10-year near 3.04%. Expectations for rate cuts continued to be scaled back, while the Federal Reserve, European Central Bank (ECB), and Bank of England all left rates unchanged but emphasized rising uncertainty around inflation and growth. In Europe, markets increasingly priced the possibility of additional ECB tightening even as Eurozone growth momentum softened.

Macroeconomic data remained mixed but generally resilient. In the U.S., payroll growth remained firm at approximately 178,000, unemployment held near 4.3%, and manufacturing activity strengthened, while core inflation remained above target. In Europe, April PMIs pointed to weaker activity, particularly in services, as higher energy prices and weaker real incomes weighed on demand.

Credit markets recovered meaningfully during April. U.S. investment grade spreads tightened 11 basis points (bps) to 78bps option-adjusted spread (OAS), while Euro investment grade (IG) tightened 15bps to 82bps OAS, broadly retracing a portion of March’s widening. The tightening reflected improved geopolitical sentiment, strong technical demand, and continued resilience in corporate fundamentals. Financials, subordinated debt, BBB-rated issuers, and shorter-dated credit outperformed, while high yield outperformed investment grade, with U.S. HY tightening 49bps to 268bps.

Despite the recovery, market leadership remained selective. In Europe, REITs, autos, lodging, and basic industry outperformed, while retail and communications lagged amid heavy issuance. In the U.S., finance companies and autos led spread compression, while technology and pharma tightened more modestly as AI-related disruption concerns remained an overhang for parts of the market. Synthetic/CDS markets lagged cash bonds, reflecting particularly strong demand for cash credit exposure.

Corporate fundamentals remained broadly supportive through the early stages of earnings season. Banks generally reported stable asset quality and resilient net interest income, while most non-financial issuers maintained full-year guidance despite heightened geopolitical and energy uncertainty. Elevated M&A activity also reinforced the importance of issuer and sector selection.

High yield and leveraged loans benefited from improving sentiment, though dispersion remained elevated. Loan markets performed strongly during the month, supported by stabilizing software performance and solid fundamentals, while higher-quality loans continued to outperform lower-tier credits. CLO issuance recovered after a softer start to the quarter.

Securitized markets also improved as rate volatility subsided and broader risk sentiment stabilized. Agency Mortgage-Backed Securities (MBS) spreads tightened approximately 8bps to around +116bps versus Treasuries, benefiting from reduced volatility and strong technical demand. The Federal Reserve continued the gradual runoff of its MBS holdings, while bank and GSE demand remained supportive. Issuance across ABS, RMBS, and CMBS markets remained robust, with many transactions heavily oversubscribed despite the higher-rate environment.

Emerging markets (EM) remained relatively stable overall, with spreads broadly returning toward pre-conflict levels in several regions, particularly Latin America. Local political developments and energy sensitivity continued to drive country-level dispersion, while oil-linked risk premia remained embedded across parts of the asset class.

Municipal markets delivered one of their strongest periods of performance in years, supported by robust inflows and favorable technical conditions, particularly in the intermediate-to-longer portion of the curve.

Overall, April marked a stabilization phase following March’s macro repricing shock. While geopolitical tensions, inflation risks, and evolving central bank expectations continued to drive volatility, markets generally demonstrated resilience, with credit spreads tightening, technical conditions remaining constructive, and risk sentiment improving across several fixed income sectors.

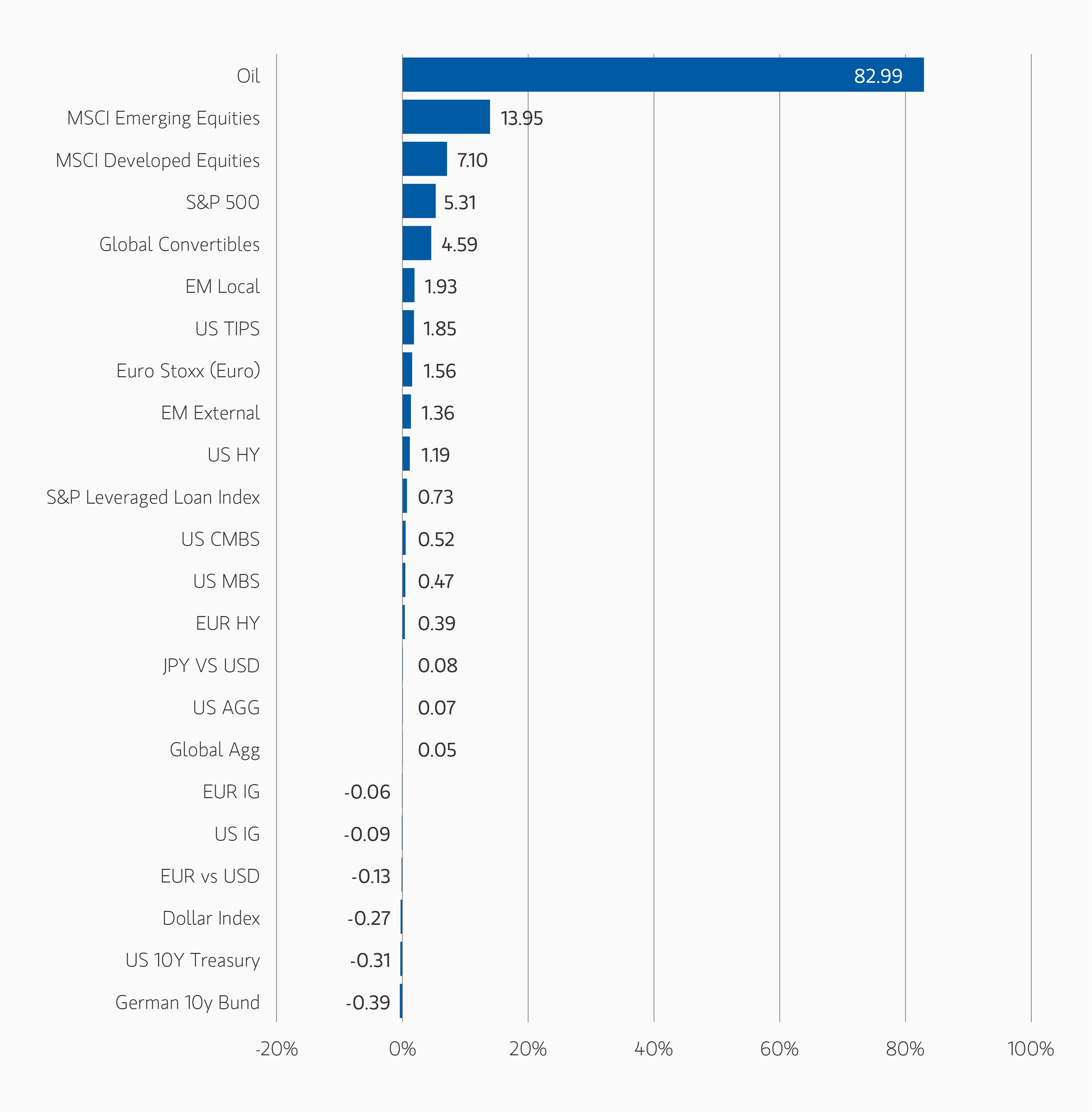

Asset Performance Year-to-Date

Asset Performance Year-to-Date

DISPLAY 1

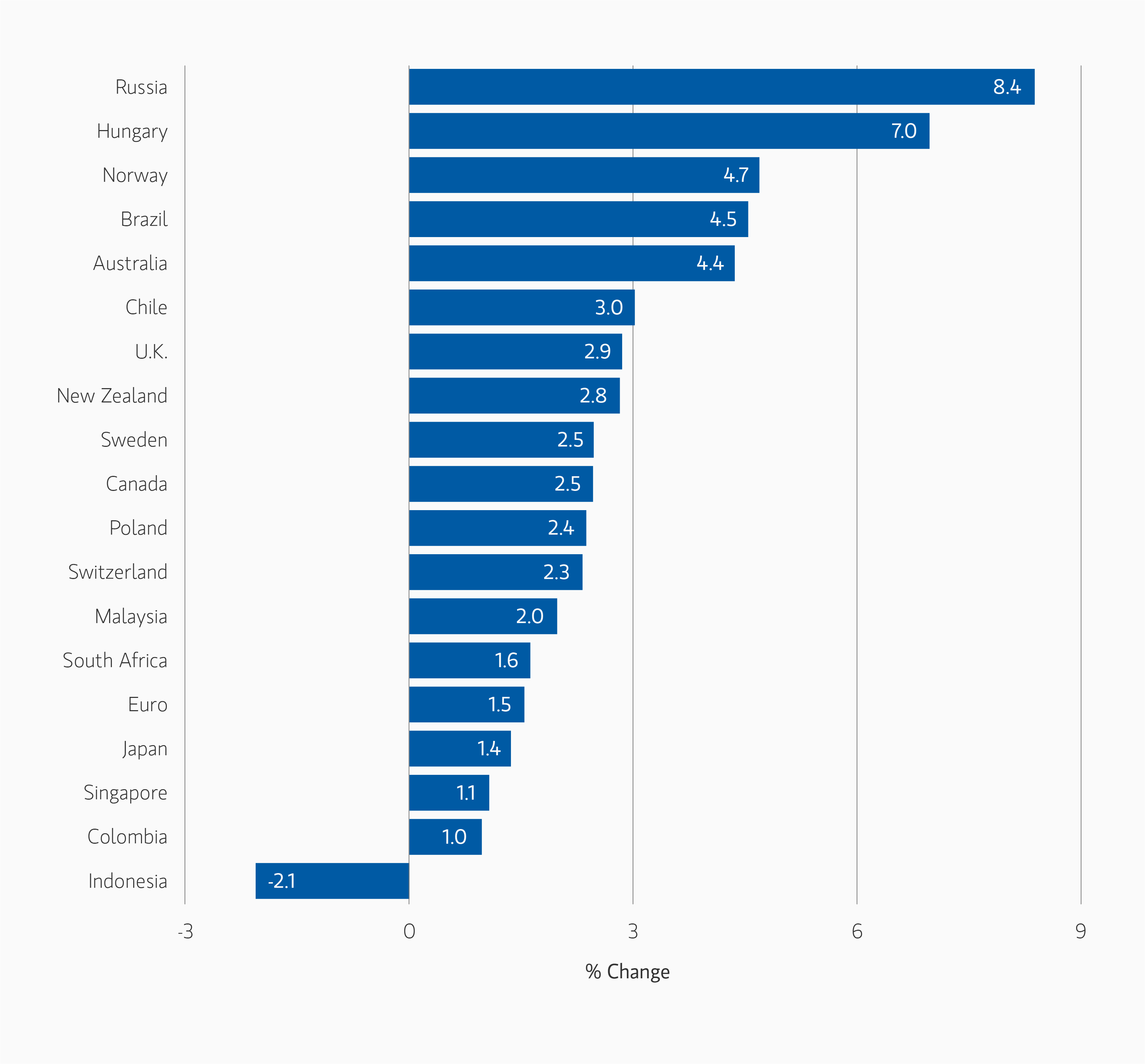

Currency Monthly Changes versus USD

Currency Monthly Changes versus USD

DISPLAY 2

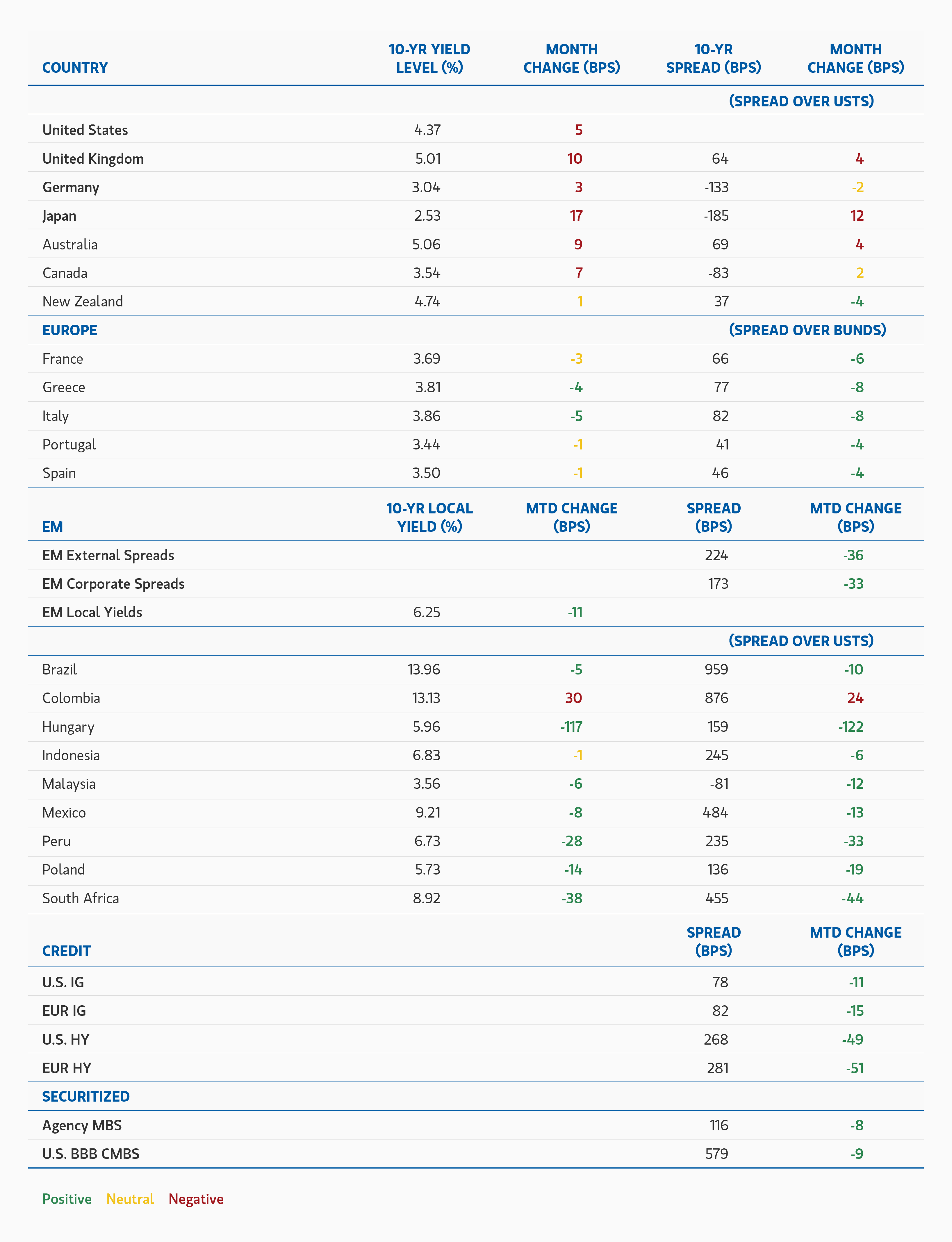

Major Monthly Changes in 10-Year Yields and Spreads

Major Monthly Changes in 10-Year Yields and Spreads

DISPLAY 3

Broad Markets Fixed Income Global Asset Allocation and Outlook

Developed Market Rate/Foreign Currency

(Long duration, neutral curve positioning)

April saw a strong reversal across developed market rates following March’s sharp macro repricing, though the backdrop remains dominated by elevated inflation uncertainty and shifting central bank expectations. While geopolitical tensions in the Middle East continued to support higher energy prices, reduced tail-risk concerns and easing volatility helped markets partially retrace the more aggressive policy repricing seen in March. Even so, central banks increased their optionality by maintaining cautious messaging, with the Fed, ECB, and Bank of England all emphasizing persistent inflation risks and limited urgency to ease policy.

We increased duration exposure in March from neutral and now maintain a modest long stance across developed markets, expressed selectively through front-end exposure in regions where growth risks appear more vulnerable to tighter financial conditions. Positioning includes longs in short-maturity Canadian and New Zealand rates, as well as U.S. Treasuries, partially offset by a small short duration position in Japan, where policy normalization dynamics and weaker technicals continue to differentiate the market.

Inflation dynamics remain central to the rates outlook. While near-term inflation expectations retraced somewhat from March extremes, longer-dated breakevens continued to move higher during April, reinforcing the view that inflation risks remain skewed to the upside if energy prices stay elevated. In response, we increased exposure to U.S. inflation-linked markets through both intermediate and longer-dated breakevens, where valuations continue to appear attractive relative to the underlying inflation backdrop.

Curve dynamics stabilized somewhat during April following the prior month’s bear flattening, and we remain neutral on outright curve positioning after exiting earlier steepening exposures.

In foreign exchange, we continue to favor selective high-beta currencies where carry remains attractive and external balances appear more resilient to elevated energy prices and tighter global liquidity conditions. Positioning remains focused on long Mexican peso exposure against both the euro and U.S. dollar. While the U.S. dollar weakened modestly during April as broader risk sentiment improved, we continue to expect FX markets to remain sensitive to geopolitical developments, energy prices, and evolving central bank expectations.

Emerging Market Debt

(Overweight)

Emerging market sovereign and corporate debt remains an attractive opportunity, supported by elevated real yields, improving fundamentals in select countries, and a more stable technical backdrop following March’s geopolitical repricing. While the conflict in the Middle East continues to keep oil-linked risk premia embedded in parts of the asset class, broader EM spreads retraced toward pre-conflict levels during April, particularly in Latin America, as volatility eased and risk sentiment improved.

Carry and income remain central drivers of expected returns, though country selection remains critical given elevated dispersion across regions. Higher energy prices continue to create divergence between commodity exporters and importers, while local political developments remain an important source of idiosyncratic risk in markets such as Hungary, Romania, the Philippines, and Indonesia.

Valuations remain attractive in select local and hard-currency markets, and many EM currencies continue to offer compelling carry relative to developed markets. We continue to favor countries with credible monetary frameworks, improving fundamentals, and attractive real yield differentials, while remaining mindful of geopolitical risks, commodity sensitivity, and evolving global policy expectations.

Corporate Credit

(Underweight IG, small overweight HY)

Our base case remains cautiously constructive for credit, even as geopolitical uncertainty and inflation risks remain elevated following the escalation of the conflict in the Middle East. The partial stabilization in markets during April, alongside signs of willingness from both the U.S. and Iran toward de-escalation, supported a recovery in risk sentiment and a retracement in spreads across both investment grade and high yield markets.

We continue to believe that a meaningful demand destruction scenario is unlikely to be the base case. Expectations for low but positive economic growth — supported by ongoing fiscal support, resilient labor markets, energy-related spending, and continued AI and infrastructure investment — remain consistent with a broadly benign default environment. Corporate fundamentals also remain healthy, though the market is increasingly entering a late-cycle phase characterized by elevated M&A activity, AI- and infrastructure-related capex, and higher shareholder distributions. This backdrop continues to reinforce the importance of sector and security selection.

At current spread levels, we continue to view carry as the primary driver of expected returns, particularly given the strong technical demand for high-quality credit and the resilience of underlying corporate fundamentals. While the near-term macro backdrop has stabilized, we continue to expect carry and security selection to remain the primary drivers of return rather than broad-based multiple expansion. Regionally, we continue to prefer Europe over the U.S., supported by relatively more balanced supply dynamics and stronger demand for high-quality carry.

We maintain a modest overweight to select high-yield issuers in both the U.S. and Europe. Although spreads tightened materially during April and issuance accelerated, fundamentals remain supportive, with improved average credit quality, manageable leverage, and contained default expectations. At the same time, elevated dispersion across sectors and issuers continues to create opportunities for selective positioning, particularly in businesses with resilient cash flows and stronger pricing power

Leveraged Loans

(Underweight)

We expect leveraged loans to remain characterized by elevated dispersion and increasingly selective technicals. While CLO demand continues to provide an important source of support for the asset class, investor preference has increasingly shifted toward higher-quality issuers and more resilient sectors. Higher-tier loans outperformed during April, while lower-rated and more cyclical credits continued to lag, reinforcing the bifurcation theme that has emerged across leveraged finance markets.

Software and technology-linked issuers stabilized during the month following earlier weakness tied to AI-related disruption concerns, though selectivity within the sector remains high. More broadly, economically sensitive sectors continue to face pressure from elevated financing costs, inflation uncertainty, and rising input costs, even as underlying corporate fundamentals remain broadly stable.

CLO issuance recovered following a softer start to the quarter, and demand for quality floating-rate exposure remains supportive. However, given the repricing in monetary policy expectations and the increasingly macro-driven market backdrop, we continue to prefer selective exposure where fundamentals remain resilient, and valuations adequately compensate for elevated dispersion and refinancing risk. While we remain underweight the asset class overall, recent spread widening and increased dispersion are beginning to create more attractive entry points in select areas of the market.

Securitized Products

(Overweight)

Agency mortgage-backed securities (MBS) and non-agency residential mortgage-backed securities (RMBS) remain a high-conviction overweight for 2026. Following the volatility experienced during March, securitized markets stabilized during April as rate volatility subsided and broader risk sentiment improved. Agency MBS spreads tightened modestly during the month, while broader securitized credit spreads remained relatively resilient despite elevated yields and ongoing macro uncertainty. Relative valuations across agency MBS continue to appear attractive versus both historical levels and other core fixed income sectors.

Technical conditions remain highly supportive across securitized markets. Demand for high-quality collateral continues to benefit from attractive all-in yields, strong money manager demand, and increasing participation from banks and GSEs as balance sheet constraints ease and relative value improves. At the same time, the Federal Reserve’s measured balance sheet runoff continues to limit net supply pressure. Although securitized products modestly underperformed corporates during April’s broader risk recovery, funding conditions and market liquidity remained strong throughout the month.

Non-agency RMBS continues to offer an attractive opportunity set, supported by stable home prices, low loan-to-value ratios, and historically low delinquency rates. Supply-demand dynamics remain favorable, with limited refinancing risk given the large proportion of borrowers locked into low mortgage rates.

Within CMBS, fundamentals remain resilient, particularly in higher-quality segments. Strong technical demand and improving sentiment continue to support selective opportunities across hospitality, logistics, storage, and high-quality multifamily assets. Issuance across ABS, RMBS, and CMBS markets has remained robust, with many transactions heavily oversubscribed, reinforcing the strength of investor demand despite the higher-rate environment.

We also remain constructive on Danish covered bonds, where defensive characteristics, strong legal frameworks, and attractive USD-hedged yields continue to support relative value.

Featured Insights