The One Big Beautiful Bill Act (OBBBA) that passed last year made several permanent and temporary tax provisions, with most taking effect in 2026. The bill’s tax and spending cuts could present both opportunities and risks for investor portfolios and personal finances.

Depending on an investor’s own goals, life events, risk tolerance, time horizon and liquidity requirements, they may consider adjusting the timing of sales or portfolio changes to better suit their tax filing preferences—for example, choosing between a standard deduction or itemizing to optimize deductions. Reviewing the portfolio and strategically deciding when to realize gains or losses is essential for helping the investor maximize their after-tax returns. Investors should consult with tax professionals to ensure that strategies are tailored to their personal circumstances and align with the new provisions.

Now that the 2025 tax filing season is over, let’s explore some key factors to keep in mind as we begin planning for the 2026 tax year.

Top tax rate and indexing for inflation

The top tax bracket is now permanent at 37% for individual incomes above $640,600 and $768,700 for married couples. The thresholds are also indexed more consistently for inflation, reducing the likelihood that modest cost-of-living increases will move investors into a higher tax bracket.

Considerations: Advisors may help investors strategically manage or defer certain income or gains to prevent exceeding limits that could place investors in a higher tax bracket.

Higher standard deductions

The Tax Cut and Jobs Act (TCJA) in 2017 doubled the standard deduction, and the OBBBA made the higher standard deduction with inflation indexing permanent. The standard deduction in 2026 will be $16,100 for single filers and $32,200 for married couples.

Considerations: Unless a taxpayer has other deductions—for example, medical expenses, mortgage interest or charitable gifts—that total more than the higher standard deduction, itemizing deductions may no longer make sense for them.

If investors anticipate gains from actions like selling a business or making Roth conversions, combining these events with a donor-advised fund (DAF) can help offset some of those gains. This approach allows investors to receive a charitable deduction that may surpass the higher standard deduction for itemizing, while providing a tax-efficient way to fulfill philanthropic goals.

Enhanced deduction for seniors

Individuals aged 65 and older are eligible for an additional deduction of $6,000, or $12,000 for married couples if both spouses meet the age requirement. This applies to earnings up to $75,000 for single filers and $150,000 for married filers, with a phase-out for income exceeding these thresholds. The deduction is available to taxpayers whether they itemize or take the standard deduction.

Considerations: Investors who are 65 and older should be made aware of the increased deduction available to them. They may want liquidate some assets for diversification, make Roth conversions or explore other planning opportunities that complement these higher deductions to take advantage of this added benefit.

Temporary state and local tax (SALT) deduction increase

The OBBBA temporarily quadrupled the state and local tax (SALT) deduction to $40,000 for married filing jointly and $20,000 for separate filers starting in 2025, from $10,000 under the original TCJA. The limit will increase 1% per year between 2026 and 2029, and the cap will revert to $10,000 in 2030.

For the 2026 tax year, the SALT deduction is $40,400. However, a phasedown provision reduces the limit by 30% if the taxpayer’s modified adjusted gross income (MAGI) exceeds $505,000. The SALT deduction limit is phased down to a minimum of $10,000 if a taxpayer’s MAGI reaches a $606,333 limit. Like the deduction limit, the threshold is halved for married filing separately.

Considerations: Higher SALT deduction limits may encourage more investors to itemize—in effect, allowing investors to take more deductions such as charitable deductions.

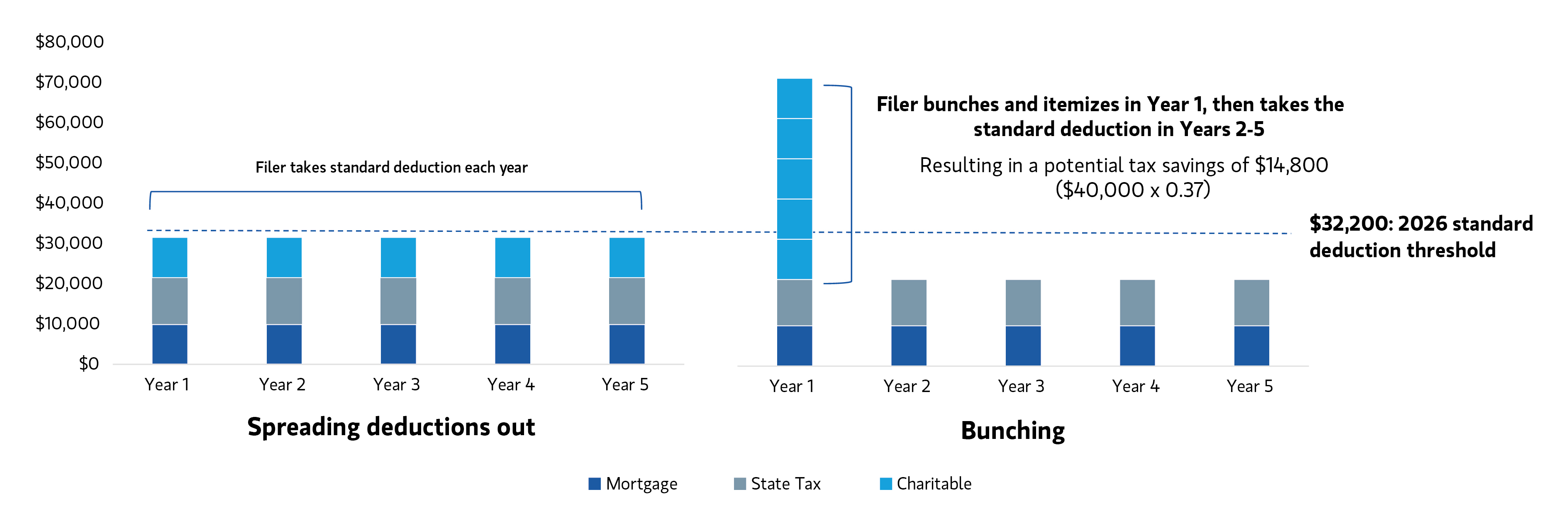

Charitable bunching with a DAF is a tax planning strategy where taxpayers concentrate multiple years of charitable donations into a single tax year. This allows them to itemize deductions in that year and then claim the standard deduction in subsequent years. This approach can be advantageous for donors who are charitably inclined, but whose annual contributions may not consistently meet the threshold for itemization.

Bunching charitable donations may yield material tax savings

Source of all tax rates: H.R.1 – One Big Beautiful Bill Act, Public Law No: 119-21 (07/04/2025). SALT deductions increased to $40,000 in 2025, with reduction if modified adjusted gross income above $500,000. The descriptions are only a summary and are not intended to provide and should not be construed as providing legal or tax advice. Each prospective donor should consult his or her own tax advisors with respect to the federal, state, local and non-U.S. tax implications of contributions.

Bunching charitable donations may yield material tax savings

Instead of donating $10,000 a year for five years, a married couple filing jointly could bunch $50,000 in a single year.

Alternative minimum tax (AMT)

AMT is a parallel tax system designed for high-income earners to ensure they pay a minimum level of tax. To determine if AMT applies, investors must compare their liability under the standard tax system with that under the AMT. This comparison excludes certain deductions, such as exercising incentive stock options (ISOs), SALT deductions or realizing large capital gains, and investors pay whichever amount is higher.

The AMT rates for the 2026 tax year remain unchanged at 26% for the first $244,500 of alternative minimum taxable income (AMTI) and 28% for any amount above that. The exemption amount is $90,100 for single filers, beginning to phase out at $500,000, and $140,200 for married couples filing jointly, with the phaseout starting at $1,000,000. Compared to 2025, the AMT exemption phaseout thresholds are 20.2% lower, at $626,350 for single filers and $1,252,700 for joint filers—meaning more high-income earners will fall into the phaseout range.

Considerations: Advisors should help investors take a multi-year approach when reviewing and adjusting income and deductions that can have an impact on AMT. Consider delaying or accelerating certain transactions, like deferring asset sales with large gains in years with higher impact.

Charitable deductions

Individuals who itemize in 2026 will have a 0.5% floor on charitable deductions, with a 35% limit for filers in the top tax rate.

0.5% floor on charitable deductions. This floor permits individuals to claim itemized deductions before the typical threshold 60% of AGI for cash contributions to a public charity, or 30% of AGI for appreciated assets.

The OBBBA also includes a set of ordering rules that specify which contribution types are subject to the 0.5% AGI floor first. For example, a donor with a $100,000 contribution base—that is, AGI without considering any charitable giving—will lose $500 of their itemized charitable deductions, while a donor with a $200,000 contribution base will lose $1,000 of itemized charitable deductions.

35% limit on itemized deduction for top tax rates. Individuals subject to the highest federal tax rate of 37% in 2026 will see itemized deductions capped at 35%. In other words, the maximum allowable tax savings from itemized deductions—such as charitable contributions, medical expenses or mortgage interest—are limited to 35%, even for those taxed at the top marginal rate. Under this new limit, for example, a taxpayer’s combined deductions of $100,000 would yield tax savings of $35,000, rather than $37,000 as before.

Non-itemizers eligible for charitable deductions. Single filers may claim up to $1,000 and married couples may claim up to $2,000 in charitable deductions. However, contributions made to DAFs and non-operating private foundations don’t qualify for this deduction.

Considerations: Advisors can evaluate the investor’s current situation and the relevant deduction opportunities to determine whether they meet certain thresholds for making a charitable gift. For individuals that are near the higher income tax brackets, they may want to access the benefits this year. DAFs can serve as an effective strategy for those seeking to maximize tax deductions while allowing the account to grow tax free for future distributions to eligible charities.

Investors who are required to take minimum distributions may also consider making a qualified charitable distribution (QCD) of up to $111,000 in 2026 to a qualifying charity. However, DAFs and private foundations are excluded from QCD eligibility.

Bottom line

Taxes play a significant role in comprehensive planning for investors. Understanding the relevant tax parameters is essential for helping investors make well-informed decisions regarding their financial strategies.

Featured Insights

Examples provided are for illustrative and informational purposes only and not intended to be reflective of results you can expect to achieve. Tax loss transactions must consider the wash-sale rule, which states that if you sell a security at a loss and buy the “substantially identical” security within 30 days before or after the sale, the loss is typically disallowed. For more information about wash sales, read IRS Publication 550. Tax saving strategies should not undermine one’s investment goals. Tax loss harvesting transactions aren’t beneficial in a retirement account because the losses generated in a tax deferred account cannot be deducted.

Contributions to charitable organizations generally cannot be rescinded or changed. Donors should be motivated by charitable intent. Charitable giving vehicles should not be treated as, and are not designed to compete with, investments made for private gain. An intention to benefit a charitable organizations should be a significant part of the decision to contribute.

The views expressed are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results.

The Firm does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Tax laws are complex and subject to change. Investors should always consult their own legal or tax professionals for information concerning their individual situations. Eaton Vance is part of Morgan Stanley Investment Management. Morgan Stanley Investment Management is the asset management division of Morgan Stanley.

Investing entails risks and there can be no assurance that Eaton Vance will achieve profits or avoid incurring losses. All investments are subject to potential loss of principal. The views and strategies described may not be suitable for all investors.

NOT FDIC INSURED. OFFER NO GUARANTEE. MAY LOSE VALUE. NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY. NOT A BANK DEPOSIT.