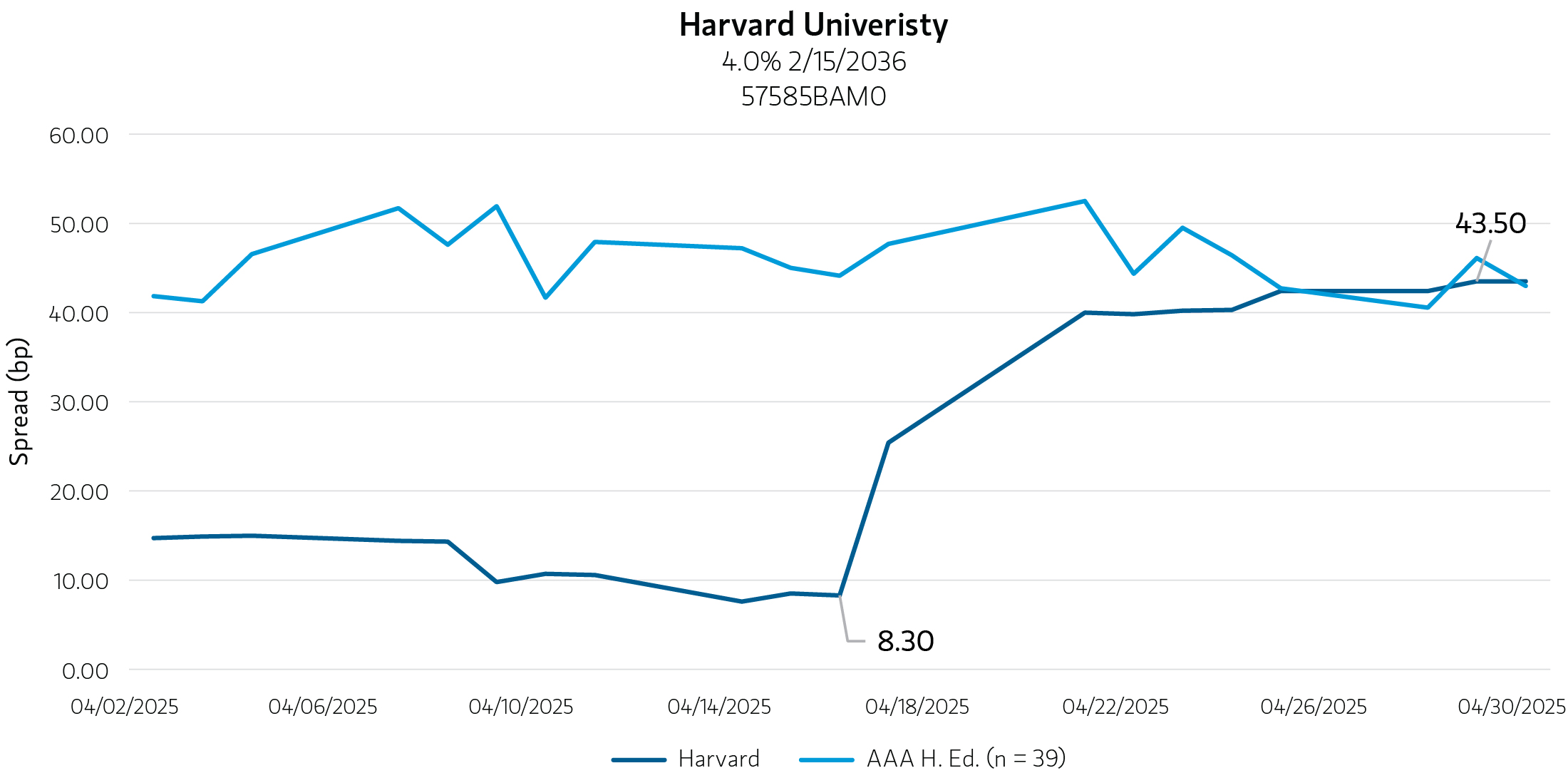

While some investors may be pricing in a political risk premium into highly-rated credits like Harvard, Harvard’s yield premium has been completely erased compared to the universe of AAA-rated higher education bonds.”

The bond ratings of universities like Harvard and Columbia are unlikely to be tarnished by threats to cut off billions of dollars in federal aid and research grants, or to revoke their tax-exempt status. With healthy finances, robust fundraising and durable demand for leading academic programs, we believe schools like Harvard are at a very low risk of default.

Last month, the federal government said it would freeze $2.2 billion in grants and $60 million in contracts to Harvard, and more to other top colleges and universities, seeking sweeping policy changes, including an overhaul of diversity and inclusion (DEI) programs, screening of international applicants, stricter crackdowns on protests and other arbitrary criteria. The Trump administration also claimed it could revoke the 501(c)(3)1 status for institutions allegedly promoting what it deems anti-American values.

Federal funding decisions must be apolitical

Executive agencies such as the Department of Education (DOE) and National Institutes of Health (NIH) have discretion over which institutions receive research grants. While these agencies may set grant conditions via regulation, delays, restrictions or by denying future funding, they it must act apolitically. Federal agencies can adjust the terms of awards through formal rule making, but any changes must comply with applicable laws (e.g. Title VI of the Civil Rights Act2), and importantly, are subject to legal challenge.

There are measures to prevent the federal government from withholding funding arbitrarily or retroactively. For example, the Impoundment and Control Act of 1974 prohibits the president from unilaterally withholding congressionally appropriated federal funds. Any attempt to intercept funds without a lawful reason or due process is likely illegal3 and subject to further review. Moreover, the 1998 IRS Restructuring and Reform Act prohibits ordering the IRS to investigate or audit specific taxpayers.

Revoking tax-exempt status requires a legal basis

There is one instance of the IRS repealing the tax-exempt status of a university on ideological grounds. In Bob Jones University v. United States (1983), the school had an internal policy prohibiting interracial dating, which the

IRS, and later the Supreme Court of the United States (SCOTUS) deemed to “violate fundamental public policy”.4 There is nothing to suggest any of the universities currently facing grant freezes have engaged in similar conduct. While there isn't a blanket prohibition against punishing specific institutions by name, legislation that singles out and punishes particular entities can face significant legal challenges in the U.S.

It is important to note that any proposed federal law to defund or tax a specific institution like Harvard or any other school need to be properly vetted. The Bill of Attainder Clause of the U.S. Constitution, which prohibits Congress from singling out an individual or institution for punishment without due process.

While some investors may be pricing in a political risk premium into highly rated credits like Harvard, Harvard’s yield premium has been completely erased compared to the universe of AAA-rated higher education bonds.5 Harvard, considered a benchmark in the market, now trades at the same level as other similarly rated credits, widening 35 basis points (bps) in just two weeks.

We view such skittish moves as reactionary selling because Harvard retains extremely sound credit fundamentals. This is evident based on several facts, including:

- 8.7x cash & investments to debt

- 9.8x cash & investments to annual operations

- $53 billion endowment ($2.58 million per full-time equivalency student)6

Harvard University 4.0% 2/15/2036

Harvard University 4.0% 2/15/2036

DISPLAY 1

Bottom Line: Harvard University maintains a high credit rating of AAA from Standard & Poor's and Moody's, indicating a very low risk of default. We believe bond markets may be overreacting in pricing Harvard and other top schools' debt. Any actions against the federal government to target universities based on perceived or alleged bias or ideology would likely face steep legal odds and would need to be examined prior to being enacted. The Trump administration also noted that it is considering revoking (or limiting) 501(c)(3) status for institutions that promote what the current administration classifies as “anti-American” values.

Featured Insights