key takeaways:

- After the post‑COVID surge in deliveries, new construction has fallen, thinning the medium‑term pipeline and setting the stage for improving fundamentals as excess supply is absorbed.

- Elevated home prices and higher mortgage rates have widened the rent‑versus‑own cost gap, extending renter tenure and supporting resilient demand.

- Valuations have adjusted and now sit below replacement cost in many markets, offering an attractive entry point

From Over Supply to Equilibrium Supply

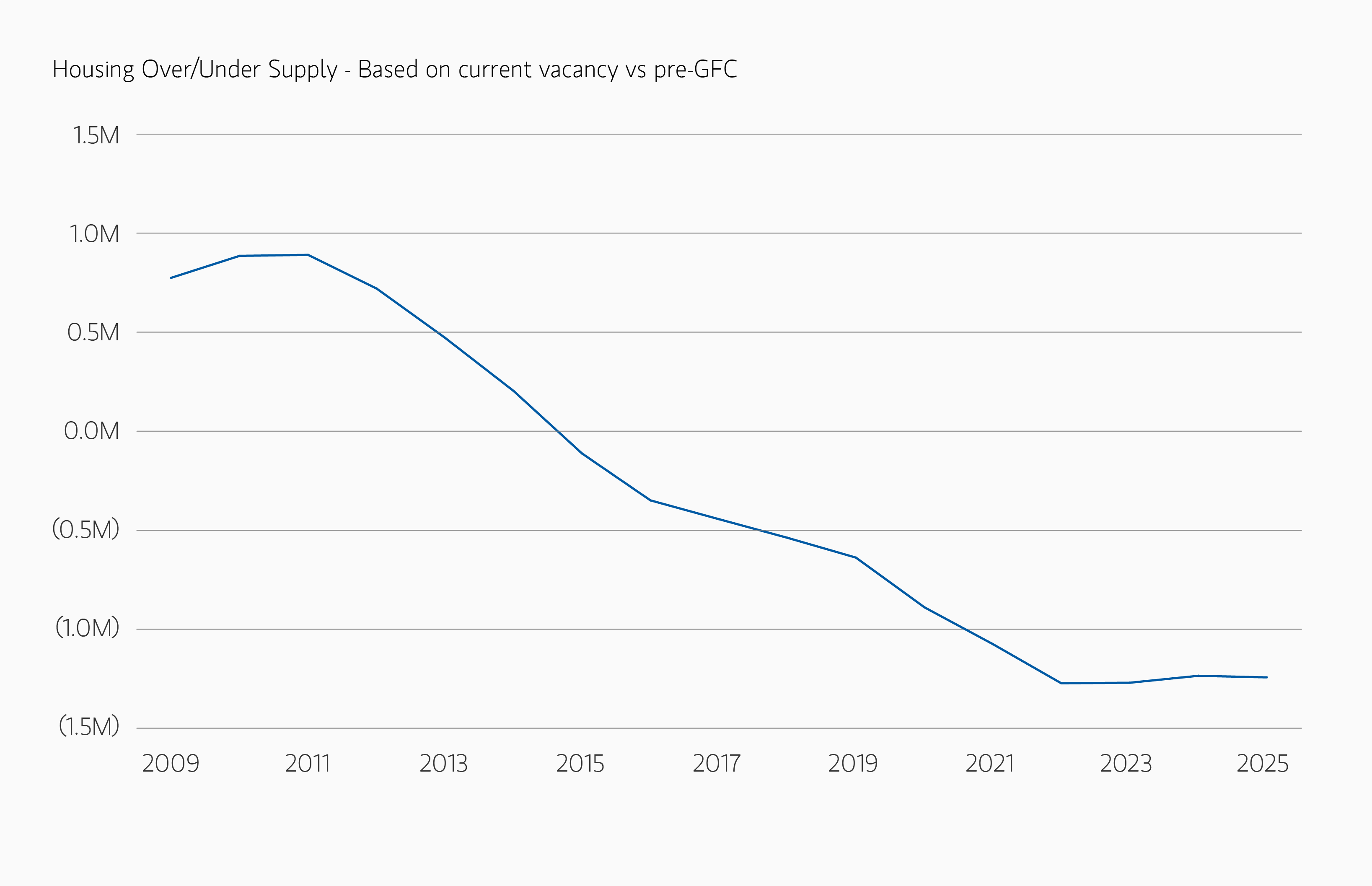

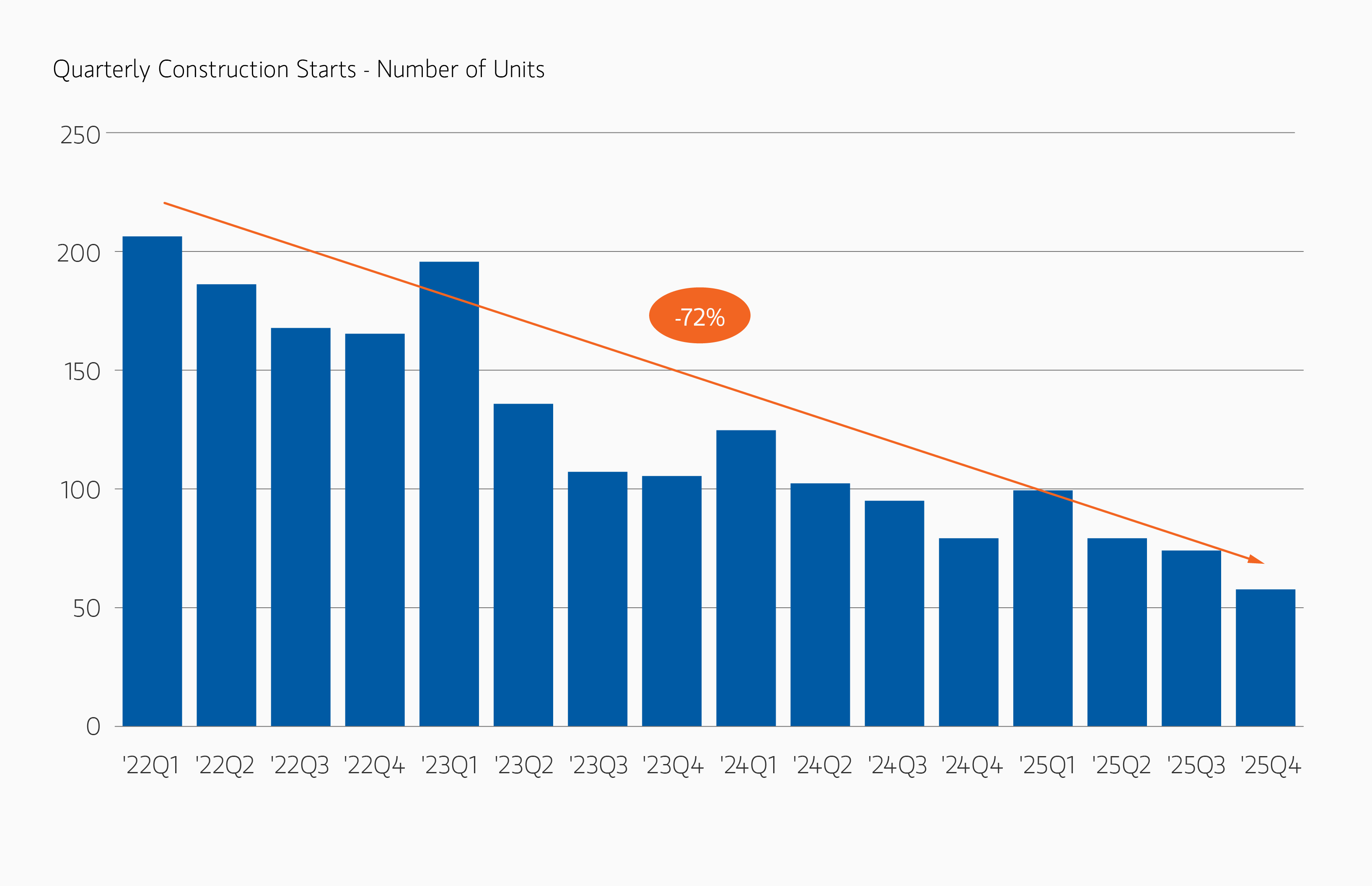

Between 2022 and 2025, 2.2 million multifamily units were delivered in the U.S. (560,000 per year on average), largely in response to outsized demand that occurred during and post-COVID. This compares to average annual deliveries of 245,000 units between 2001 and 2020. The ensuing spike in inflation, construction costs, and interest rates have contributed to a significant decline in new construction starts, down 50% nationally from 2023 levels. Therefore, while the residual effects of post-COVID excess supply have put pressure on rents in some submarkets, the medium-term pipeline has thinned materially. Additionally, this pullback in new supply is occurring against a backdrop of underbuilding since the GFC in many U.S. housing markets, particularly in urban and infill locations.

Prevalent Housing Shortage

Source: Census Bureau, MSREI Strategy, as of December 2025

Prevalent Housing Shortage

Multifamily Construction Continues to Fall

Source: Costar, MSREI Strategy, as of December 2025

Multifamily Construction Continues to Fall

Durable Demand Drivers Supported by For-Sale Affordability Challenges

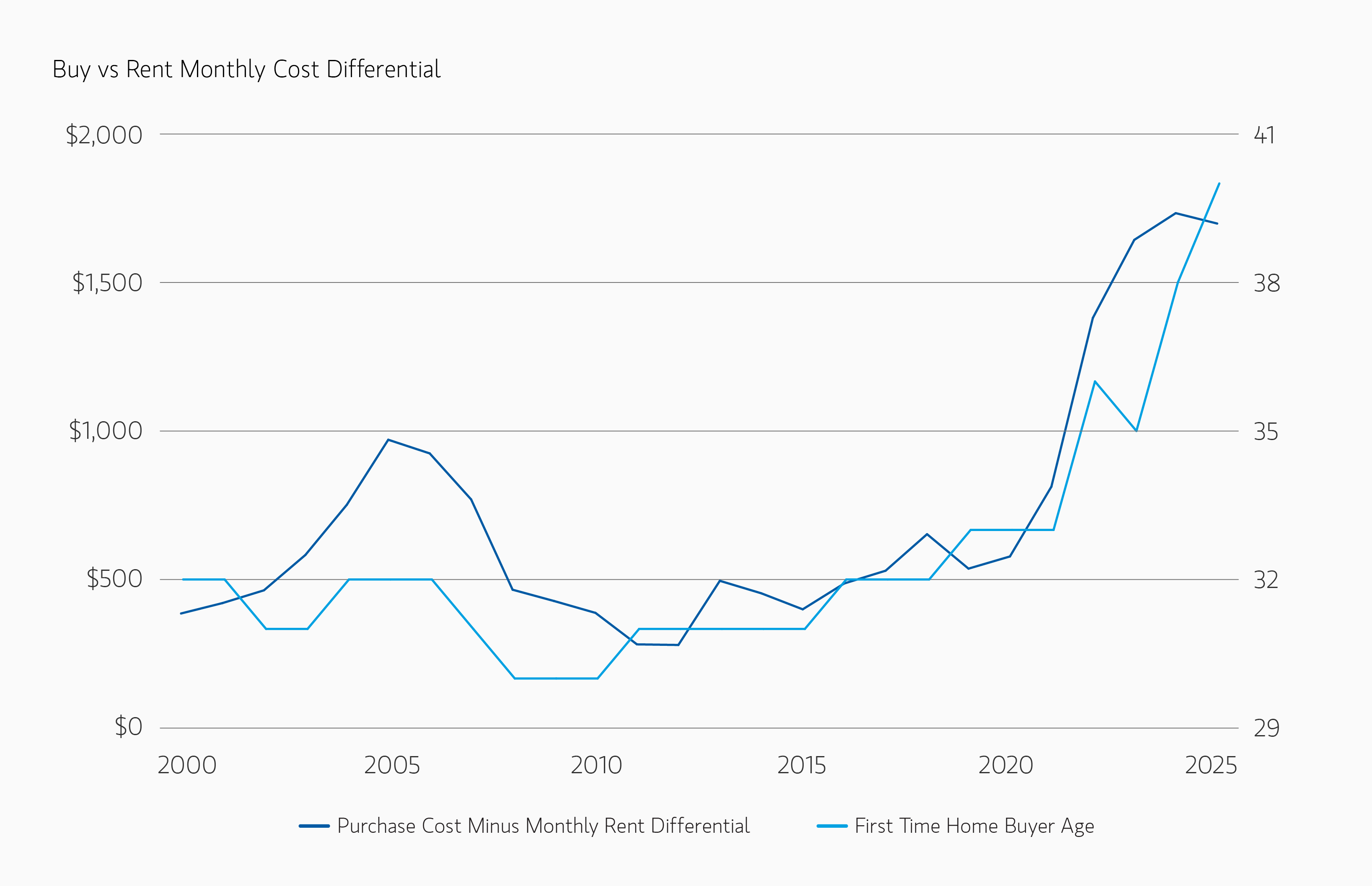

Historically, multifamily demand has been correlated with cyclical growth in household income, which is expected to remain robust and above 4% over the next five years. Additionally, demand is increasingly anchored by structural affordability constraints in the for sale housing market. Elevated home prices, higher mortgage rates, and limited existing home inventory have materially widened the cost differential between owning and renting. This has extended renter tenure, supported renewal rates, and reduced elasticity of demand even amid slower job growth. Challenged for-sale affordability is expected to create 2.5 million1 new renter households from 2025 to 2028 as the home ownership rate declines from 65.6% to 64.7%.

Demographic trends further reinforce this dynamic. Large renter cohorts continue to move through prime renting years, while older households increasingly opt for rental housing due to mobility, lifestyle, and capital preservation considerations. The result is a demand base that is broad, sticky, and less cyclical than in past cycles.

Unaffordable For-Sale Market Supports Renting

Source: John Burns, NAR, MSREI Strategy, as of December 2025

Unaffordable For-Sale Market Supports Renting

Income Growth Supports Rent Growth

Source: Greenstreet, MSREI Strategy, as of December 2025

Income Growth Supports Rent Growth

Inflation Hedge and Durable Income Help Mitigate Market Volatility

Multifamily has historically delivered durable and stable income supported by a diversified tenant base. These defensive attributes are increasingly valued in the current environment of elevated geopolitical risk. Its inflation hedging characteristics are enhanced by relatively short lease durations, which allow rents to re-price more frequently in rising cost environments, as evidenced during the most recent inflationary cycle. While other sectors face secular demand challenges or technological disruption, multifamily performance remains closely tied to fundamental human needs—housing, affordability, and proximity to employment and services. This has helped drive more resilient demand, even during economic downturns, as affordability pressures and higher interest rates encourage households to rent more by necessity.

Strong Inflation Hedge due to Shorter Duration Leases

Source: Costar, Oxford Economics, MSREI Strategy as of January 2026

Strong Inflation Hedge due to Shorter Duration Leases

Lower Volatility due to Diversified Tenants and Needs-Based Demand

Source: NCREIF, MSREI Strategy, as of November 2025

Lower Volatility due to Diversified Tenants and Needs-Based Demand

Reset Pricing Provides Attractive Entry Point

The rapid rise in interest rates from 2022 to 2024 drove a meaningful repricing across real estate, including multifamily, where transaction prices fell by 20%, according to Real Capital Analytics. The ability to acquire at a reset basis below today’s replacement cost represents an attractive entry point for investors, particularly with the expectation that replacement cost is unlikely to decline over the intermediate term. The attractiveness of reset prices is further bolstered by a more favorable financing environment. Tighter lending spreads due to the depth of multifamily lenders and lower base rates have created more attractive debt. This has spurred transaction activity as both buyers and sellers have recalibrated pricing expectations.

Multifamily Transaction Volume is Increasing

Source: Real Capital Analytics, March 2026

Multifamily Transaction Volume is Increasing

Conclusion

We believe durable needs based demand and a reduced supply outlook support a recovery in multifamily fundamentals over the near to medium term. Improving liquidity and opportunities to acquire high quality assets below current replacement cost further enhance the attractiveness of U.S. multifamily investments.

Featured Insights